Using a limited company (commonly set up as a Special Purpose Vehicle or “SPV”) has its advantages:

- Tax efficiency – profits are subject to corporation tax, which may be more favourable depending on your income bracket.

- Flexibility for reinvestment – easier to reinvest profits into future property purchases without incurring personal tax first.

- Long-term planning – can allow for more efficient inheritance and capital gains planning.

The trade-offs include:

- Setup and running costs – accountancy fees, compliance charges, bank fees, and Companies House filing obligations.

- Mortgage considerations – limited company mortgage rates are usually higher than personal ones.

- Director responsibilities – you will need to act as a director and comply with company law.

- Personal guarantees – lenders typically require directors to give personal guarantees when borrowing through a limited company.

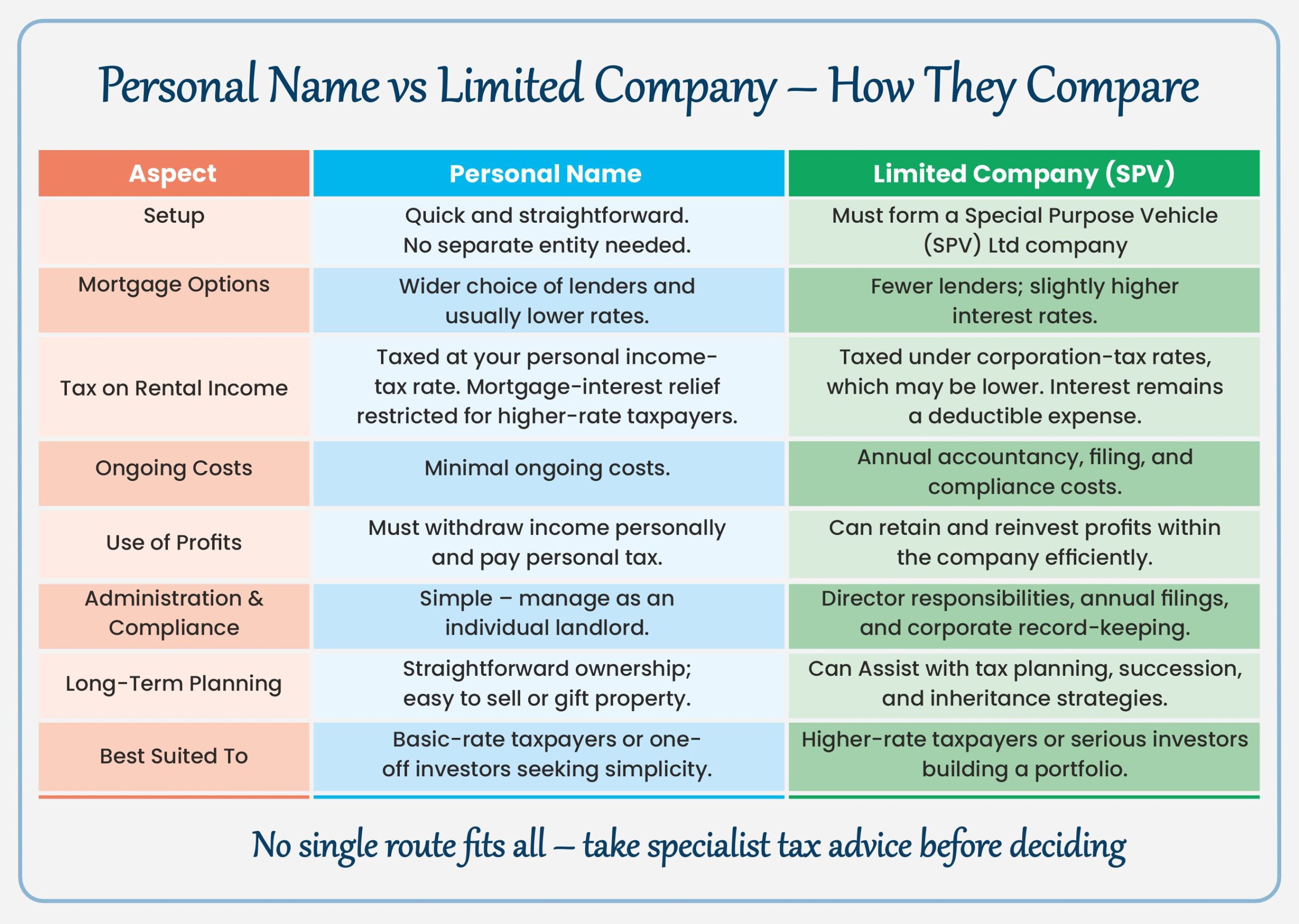

At a Glance – How Personal Name and Limited Company Ownership Compare

To help summarise the key differences, the infographic below provides a quick visual comparison of both routes.

- Annual filings with Companies House (confirmation statements, statutory accounts).

- Corporation tax returns and ongoing accountancy costs.

- Acting as a director/shareholder and ensuring compliance with company law.

Personal guarantees: even if the mortgage is in the limited company’s name, most lenders will require the directors to personally guarantee the loan. This means that if the company defaults, your personal assets may still be at risk.

Your end goal should influence the decision. For example:

- If you plan to sell the property and cash out the gains, your tax route may look different in personal names versus a company.

- If your plan is to retain and pass on the property, limited companies can sometimes help with inheritance planning and structuring shares.

- If your plan is simply to earn rental income during retirement, personal names may be simpler and more cost-effective.

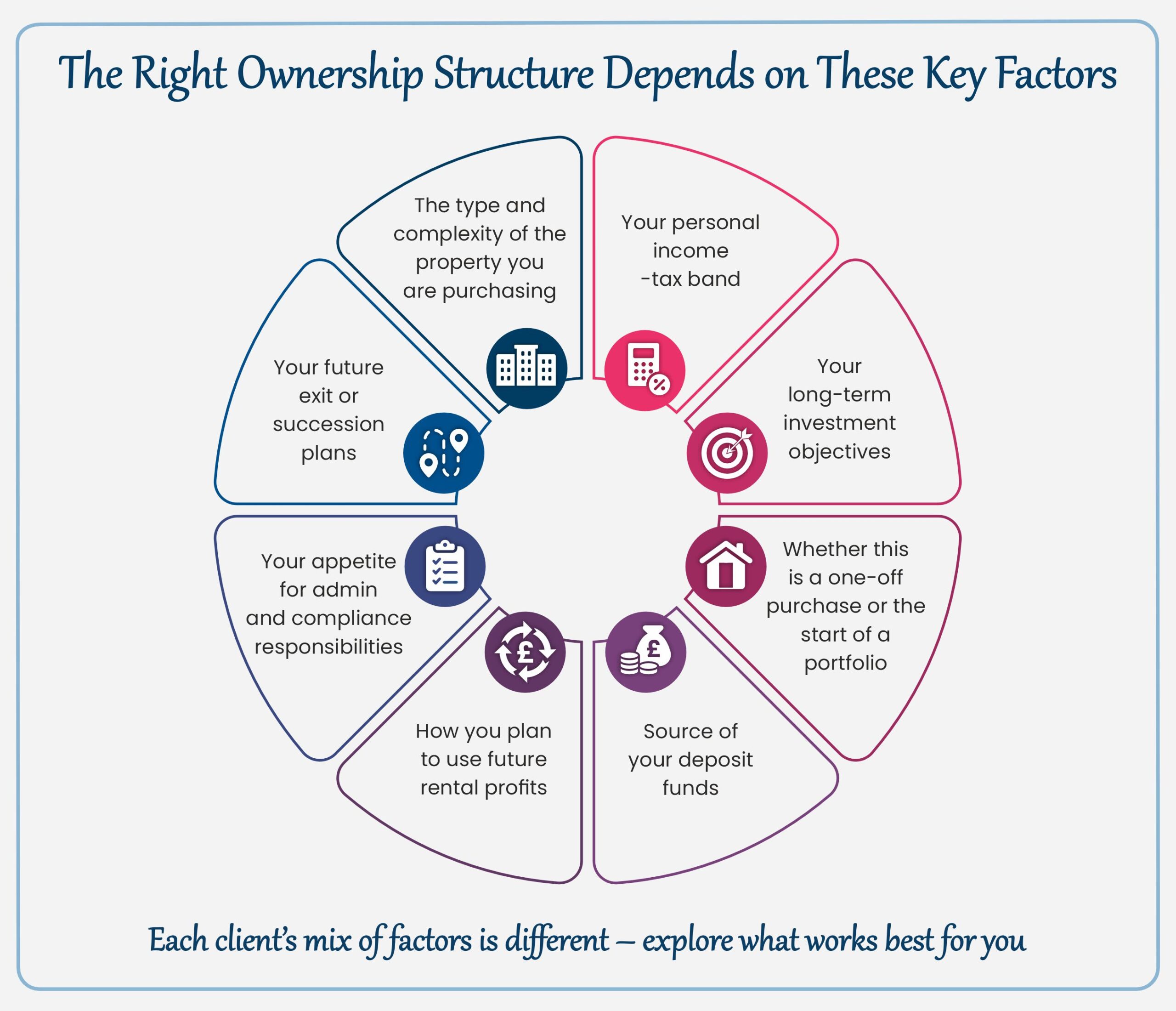

Choosing the right structure depends on a combination of factors. The infographic below outlines the key elements that typically influence what works best for each client

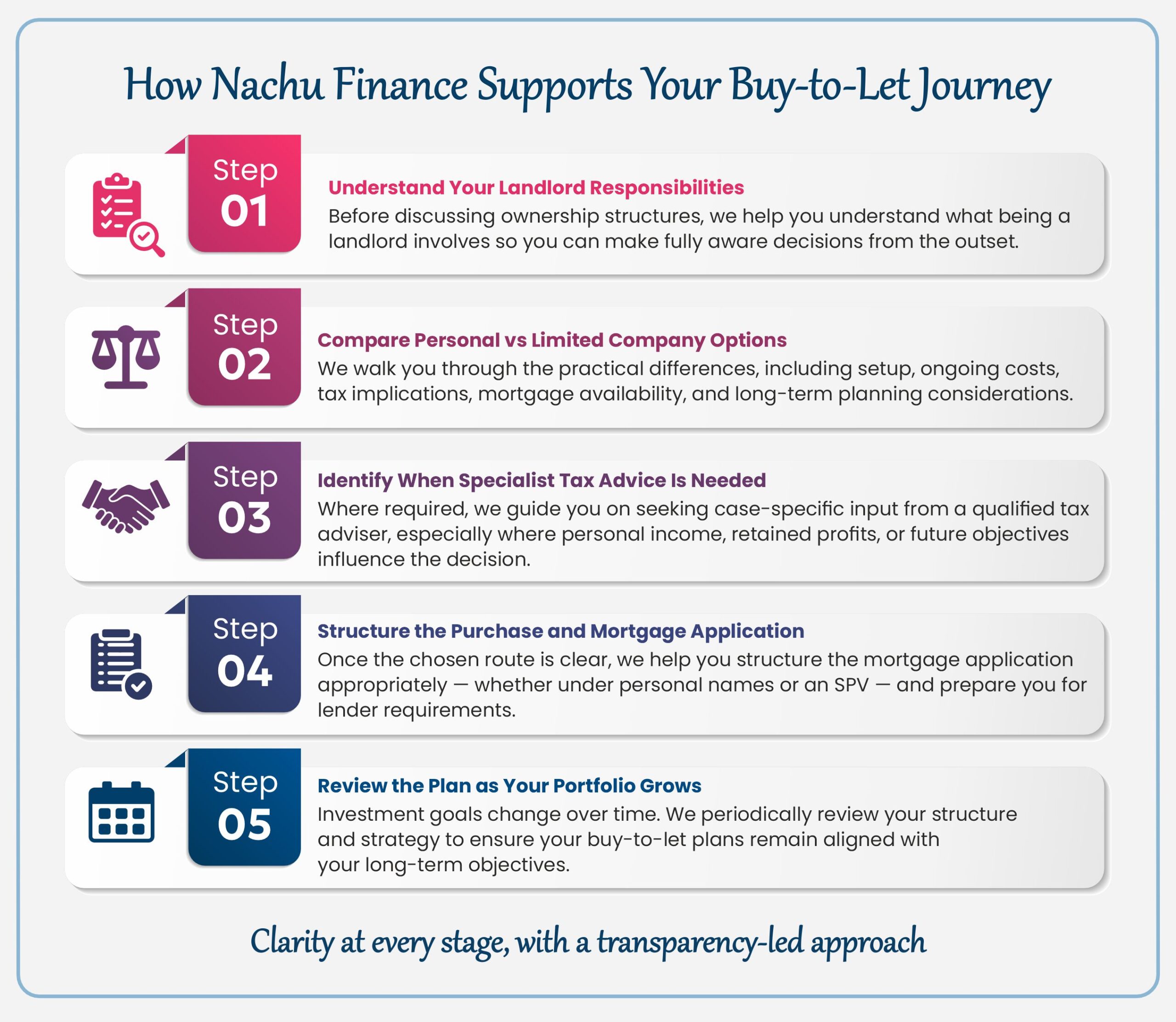

At Nachu Finance, our role is to guide you through every stage of your buy-to-let planning with clarity and structure.

We start by ensuring you fully understand what it means to be a landlord, then help you compare the practical differences between personal ownership and using a limited company.

Where a tax specialist’s input is needed, we point you in the right direction so your decision is made with complete confidence.

Once the structure is clear, we help you position the mortgage application correctly and follow through with the paperwork, lender requirements and timelines. As your plans evolve, we continue to review your approach so your strategy remains aligned with your long-term goals.