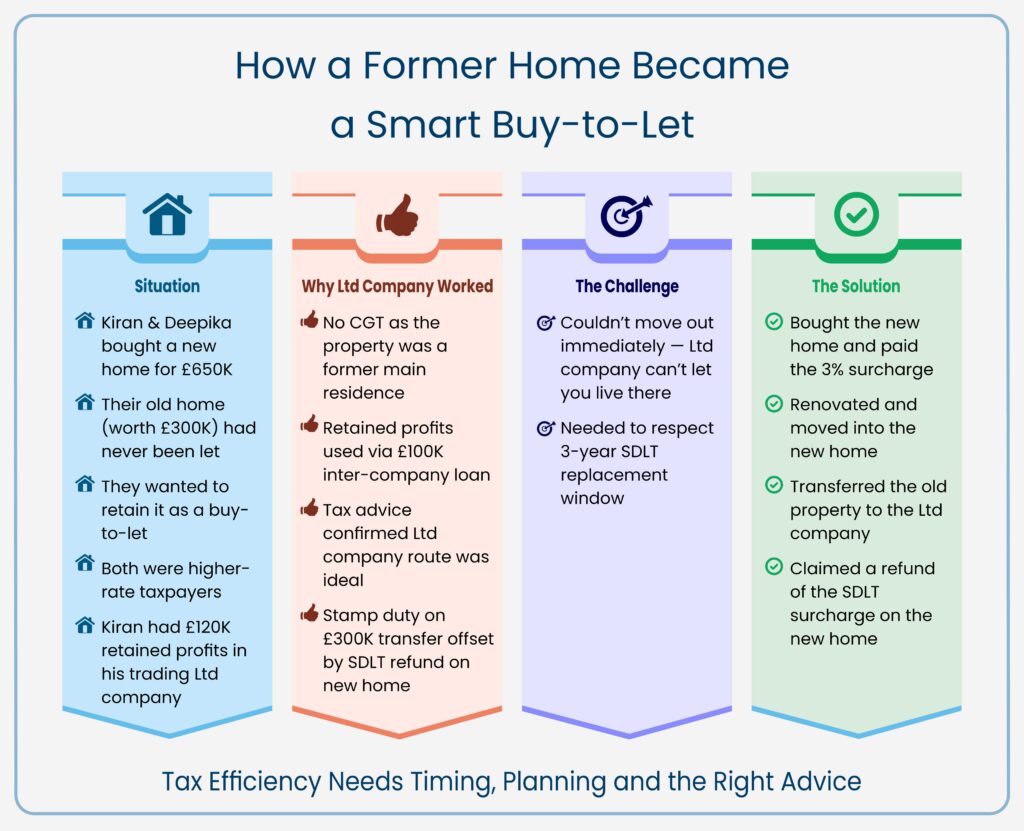

Kiran and Deepika were in the process of purchasing a new residential property in 2024, priced at £650,000. At the time, the additional stamp duty surcharge was still 3%, just before it increased to 5%. Both were higher-rate taxpayers, and they had carefully planned their next move with tax efficiency in mind.

Their existing property—valued at £300,000—had never been let out and had always been Kiran’s primary residence. While they had no intention of selling it, they also didn’t want to hold it personally as a buy-to-let due to the tax inefficiencies.

Kiran, an IT contractor, had £120,000 in retained profits in his trading Ltd company. After consulting with their accountant, it was clear that using a Ltd company structure for the buy-to-let was the right option for their circumstances.

As part of the transaction, £100,000 of the retained profits was used towards the property purchase, structured as an inter-company loan from the trading business to the new property investment company. This helped minimise personal capital outlay and allowed tax-efficient use of existing funds.