- What is the maximum loan available to you?

- What deposit is needed and where will it come from?

- What one-off costs are likely at the start?

- What will your monthly payments look like under realistic options?

What we capture from you:

- Employment and income details (including bonuses, overtime, or commissions).

- If self-employed or a company director — profits, salary, dividends, latest accounts, or SA returns.

- Credit commitments such as loans, cards, car finance, or student loans.

- Family situation and foreseeable changes affecting affordability.

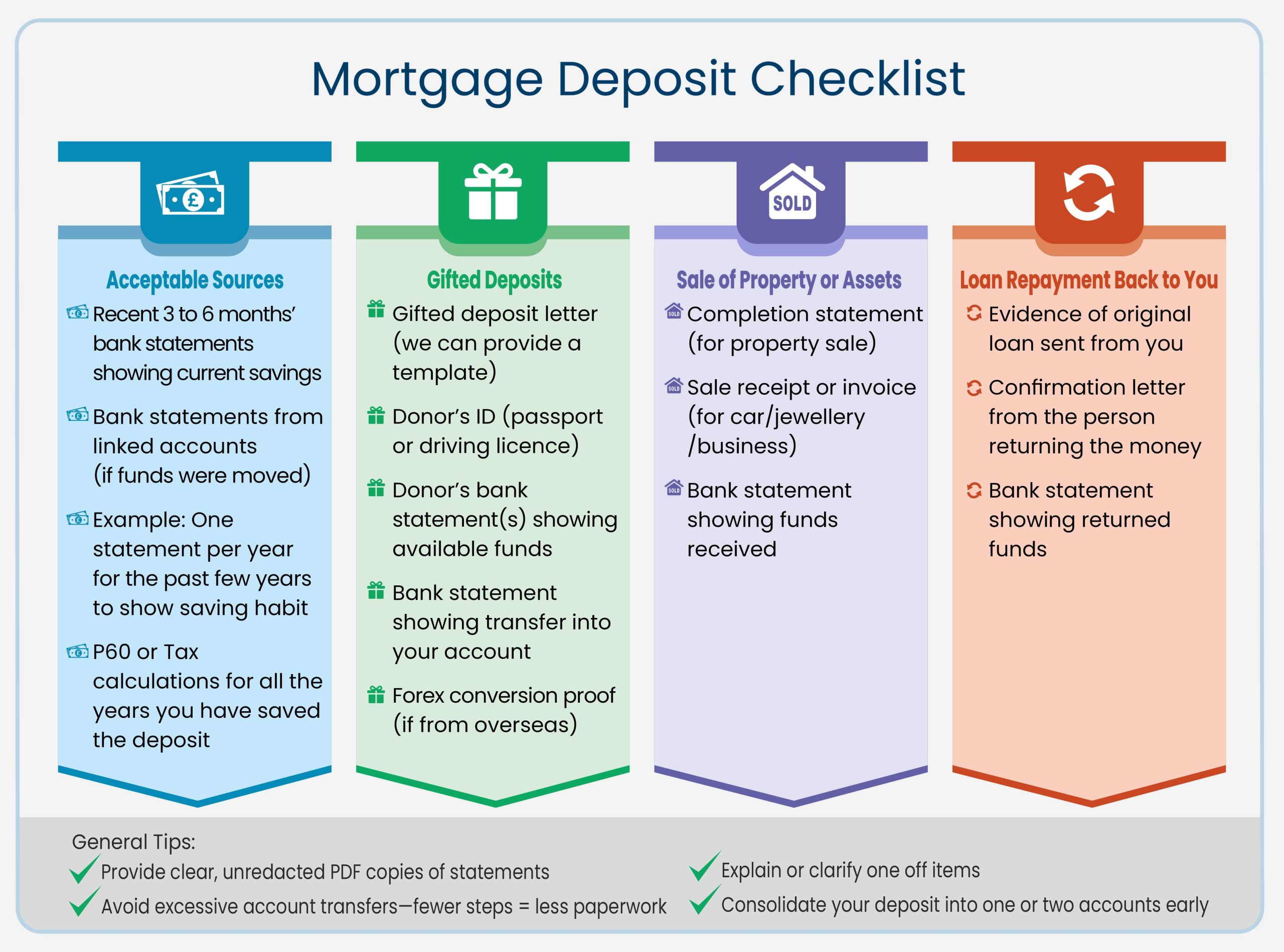

- Deposit source and evidence.

- Property preferences such as freehold or leasehold, service charges, ground rent, or new-build details.

Our unique approach

We prepare a personalised, dynamic spreadsheet that models:

- Different property prices and deposits.

- The impact of term or rate changes.

- How your affordability and payments shift with each scenario.

This prevents wasted viewings and helps you and your family align on a realistic plan before falling in love with a property outside budget.

Outputs you receive:

- A clear headline range for purchase price and loan.

- Estimated upfront costs.

- Indicative monthly payments under a few realistic setups.

- A summary of the best-case pathway, subject to standard checks.

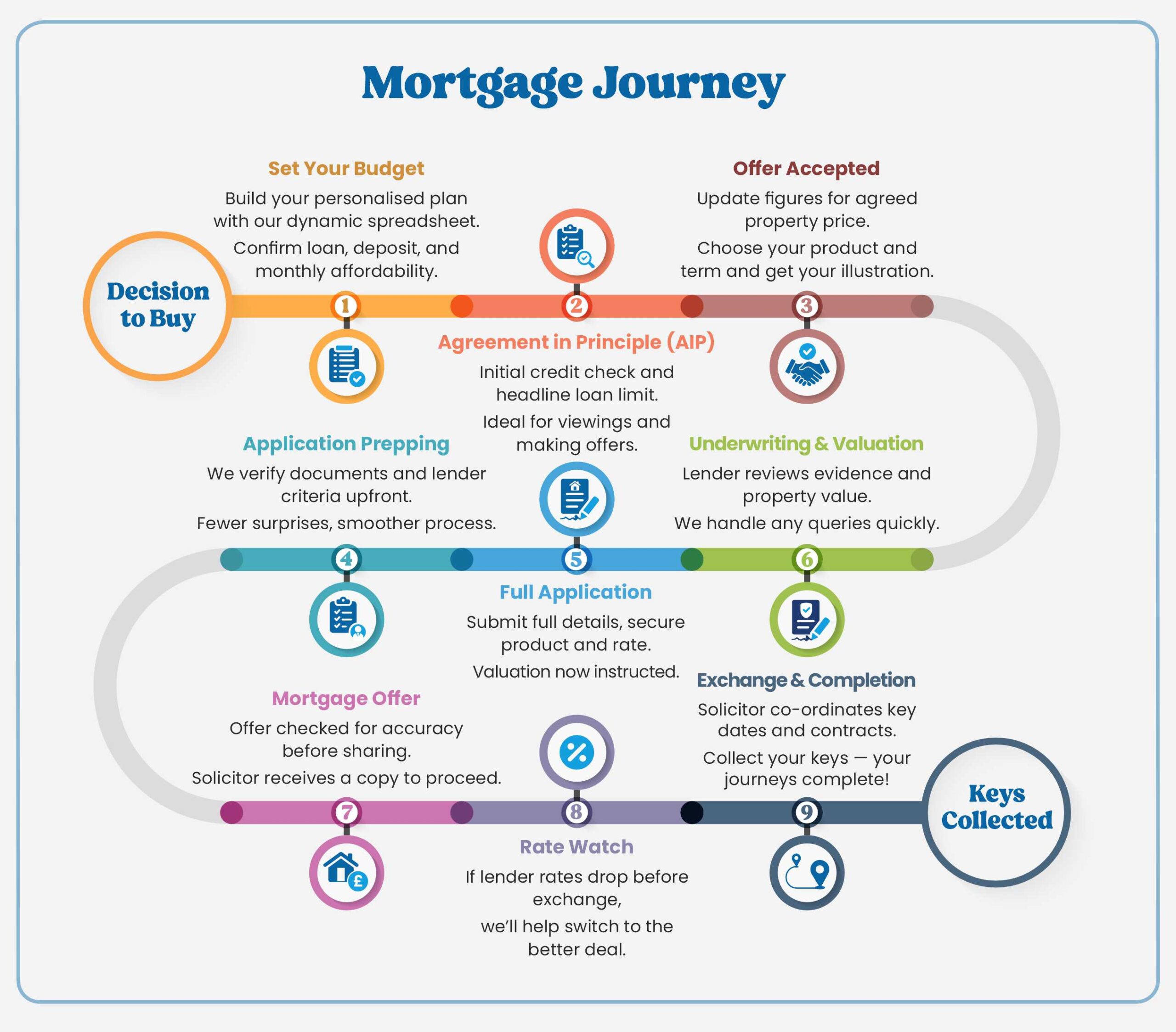

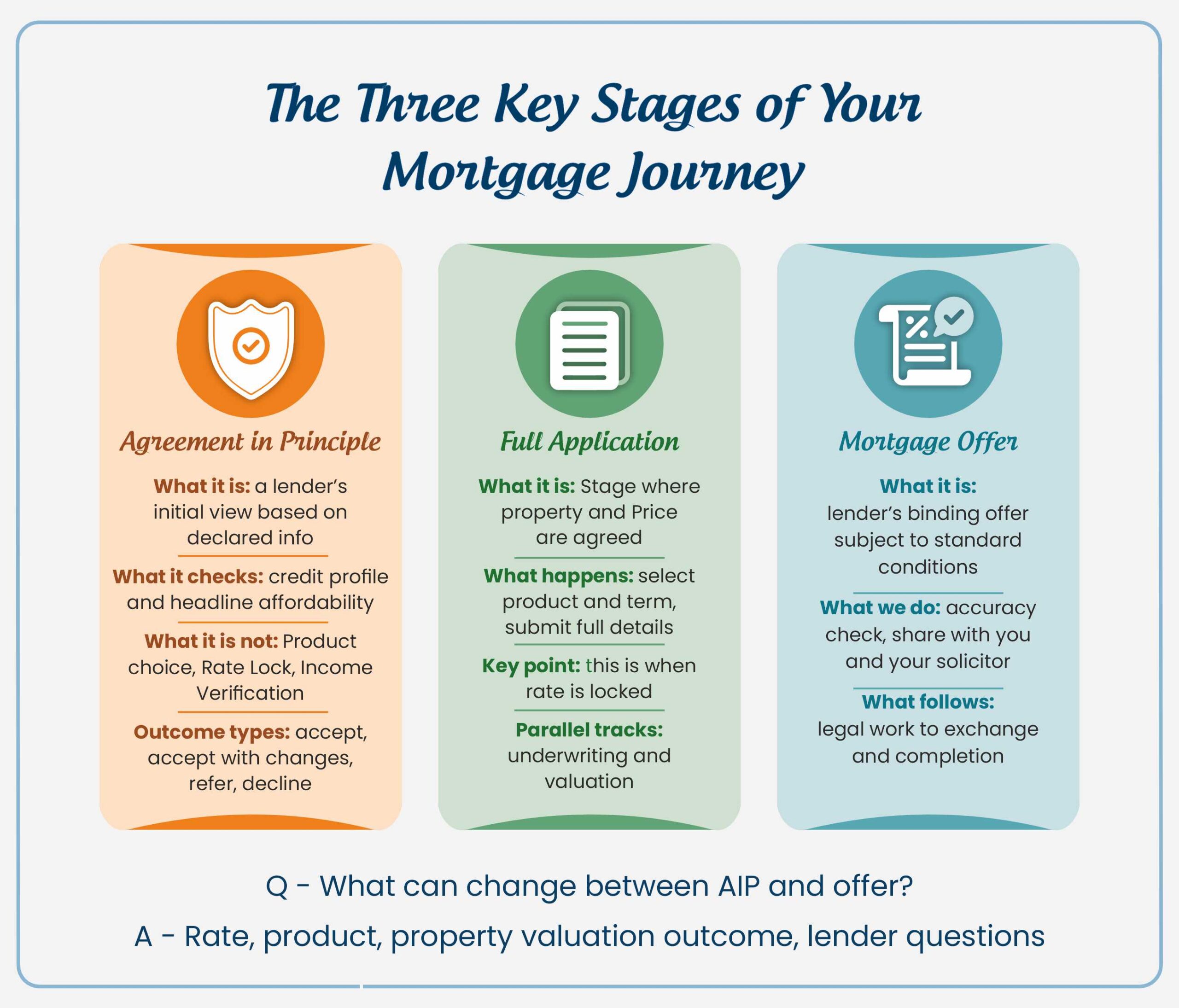

Only after the property and price are agreed. Before that, we show you ranges and examples — not specific products.

Once an offer is accepted, we refresh your spreadsheet and review:

- Product style (fixed, tracker, discount).

- Fixed period (two or five years, and whether flexibility is important).

- Term, affordability, and how it affects long-term cost.

- Fees and whether adding or paying upfront makes sense.

- Leasehold and property-type considerations.

The key document you receive:

A detailed Mortgage Illustration that outlines your rate, fees, term, payments, and deposit.

This forms the foundation of the final mortgage offer, assuming there are no material changes.

- ID and address verification.

- Income documents: latest payslips, P60s for the last two years, and employment letter if required; or SA302s (Tax Calculations), Tax Year Overviews, company accounts, and accountant references for business owners.

- Bank statements and explanations for unusual transactions.

- Evidence of all credit commitments and deposit source.

- Property details (lease, ground rent, new build warranty, etc.)

Why this matters:

It reduces back-and-forth, makes underwriting smoother, and surfaces deal-breakers early when there’s still time to adapt.

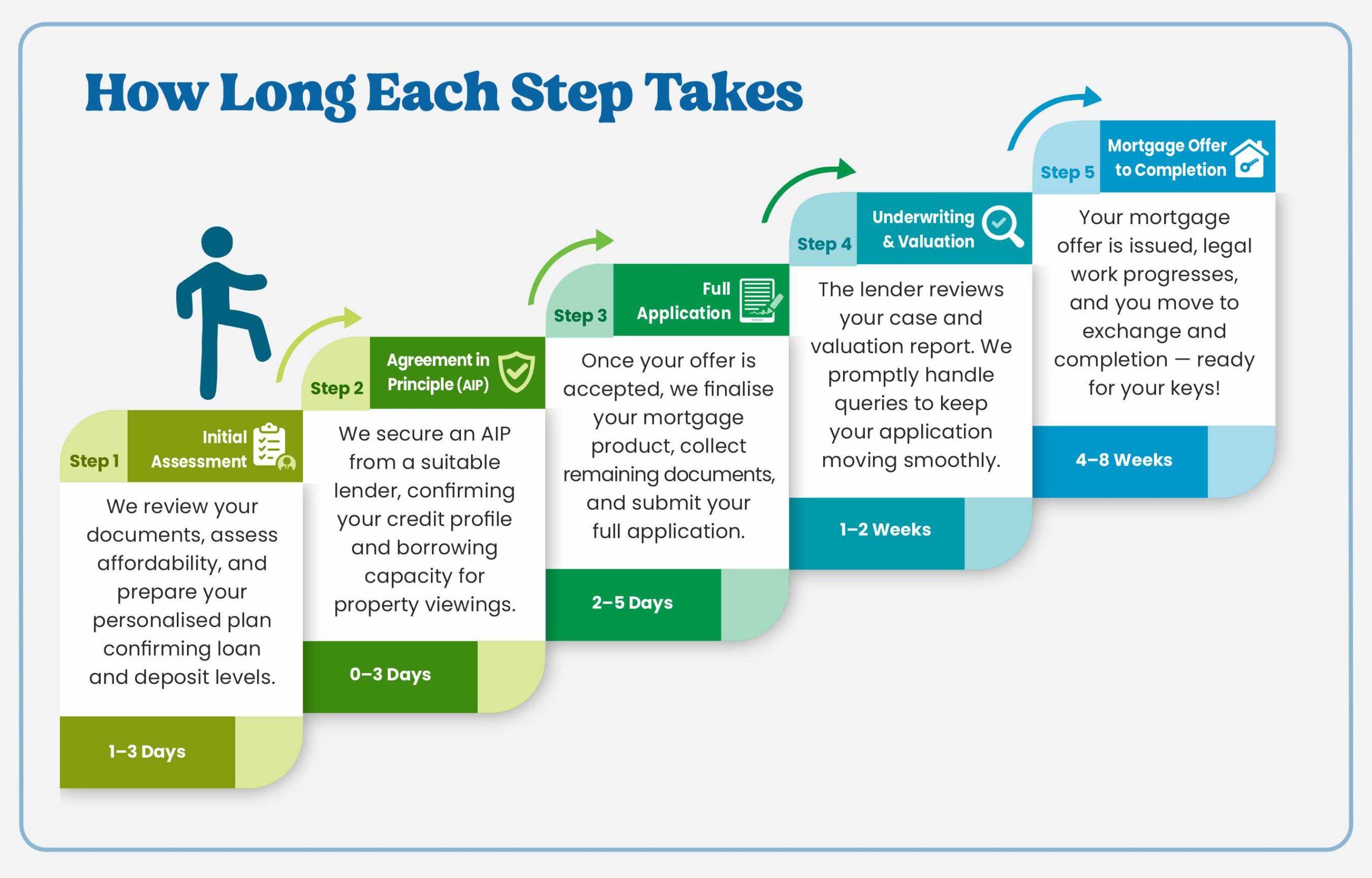

- The case manager checks that all documents match the application.

- Queries are common; some cases complete in a single round, while others require several iterations depending on complexity.

- The lender focuses on identity, affordability, credit conduct, and how your deposit is sourced and evidenced.

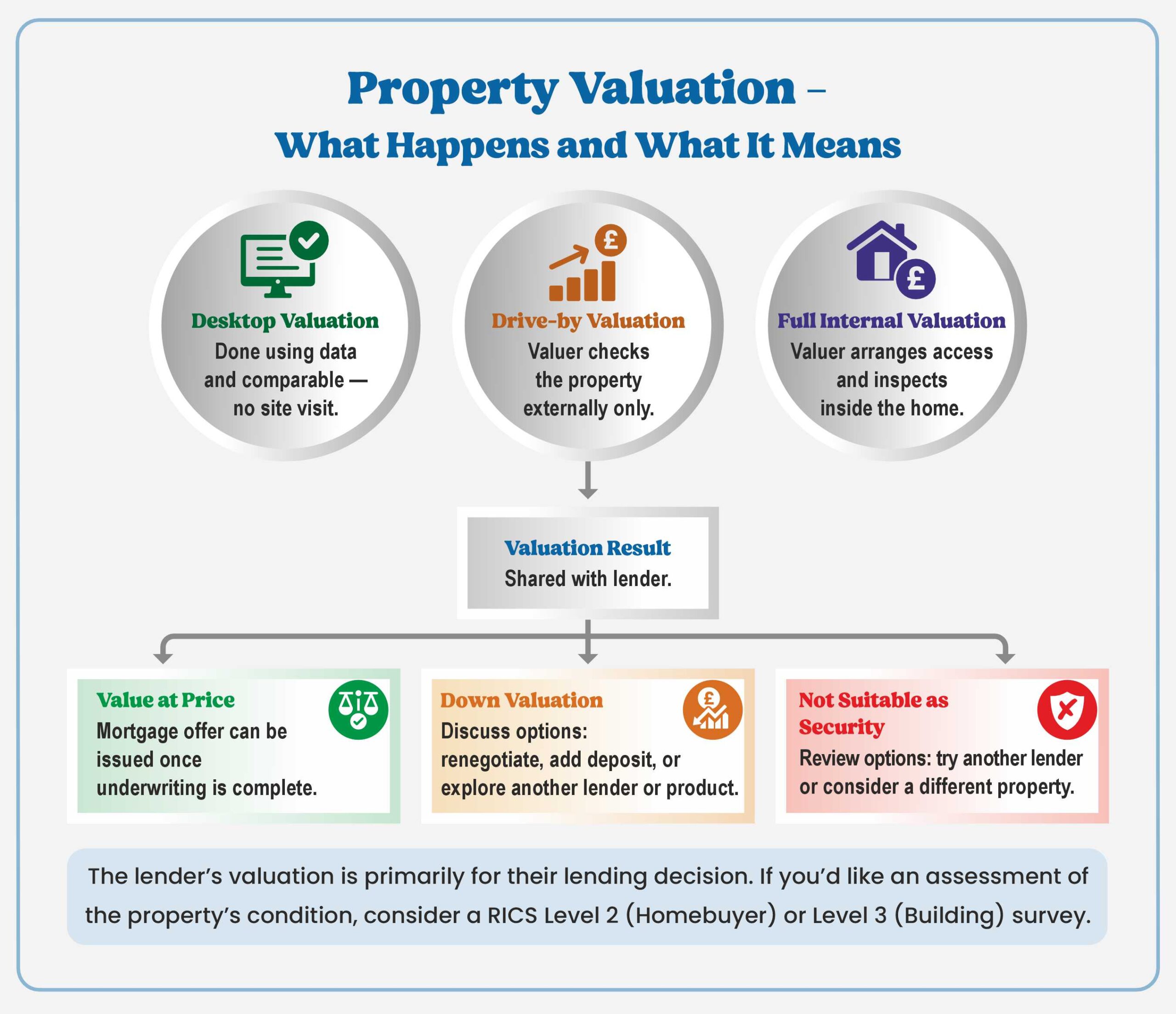

Valuation — types, triggers and outcomes:

At this point, the lender instructs a valuation to confirm that the property is suitable security for the mortgage and that its value matches the agreed price.

You may not always see a valuer in person — sometimes it’s done digitally or from outside the property.

The infographic above shows the three main valuation methods and the possible outcomes.

Here’s how to read it in context:

- If the valuation comes back at the agreed price, the process moves smoothly to mortgage offer.

- If it’s lower than the purchase price (a “down valuation”), we’ll discuss options — renegotiating the price, increasing your deposit, or exploring alternative lenders.

- If the property is deemed unsuitable as security, this usually points to structural or legal issues. In such cases, we’ll reassess whether another lender or property is more appropriate.

If you’d like to understand the different types of property surveys and when each is recommended — for example, a RICS Level 2 (Homebuyer) or Level 3 (Building) report — read our detailed guide:When to Get a Property Survey