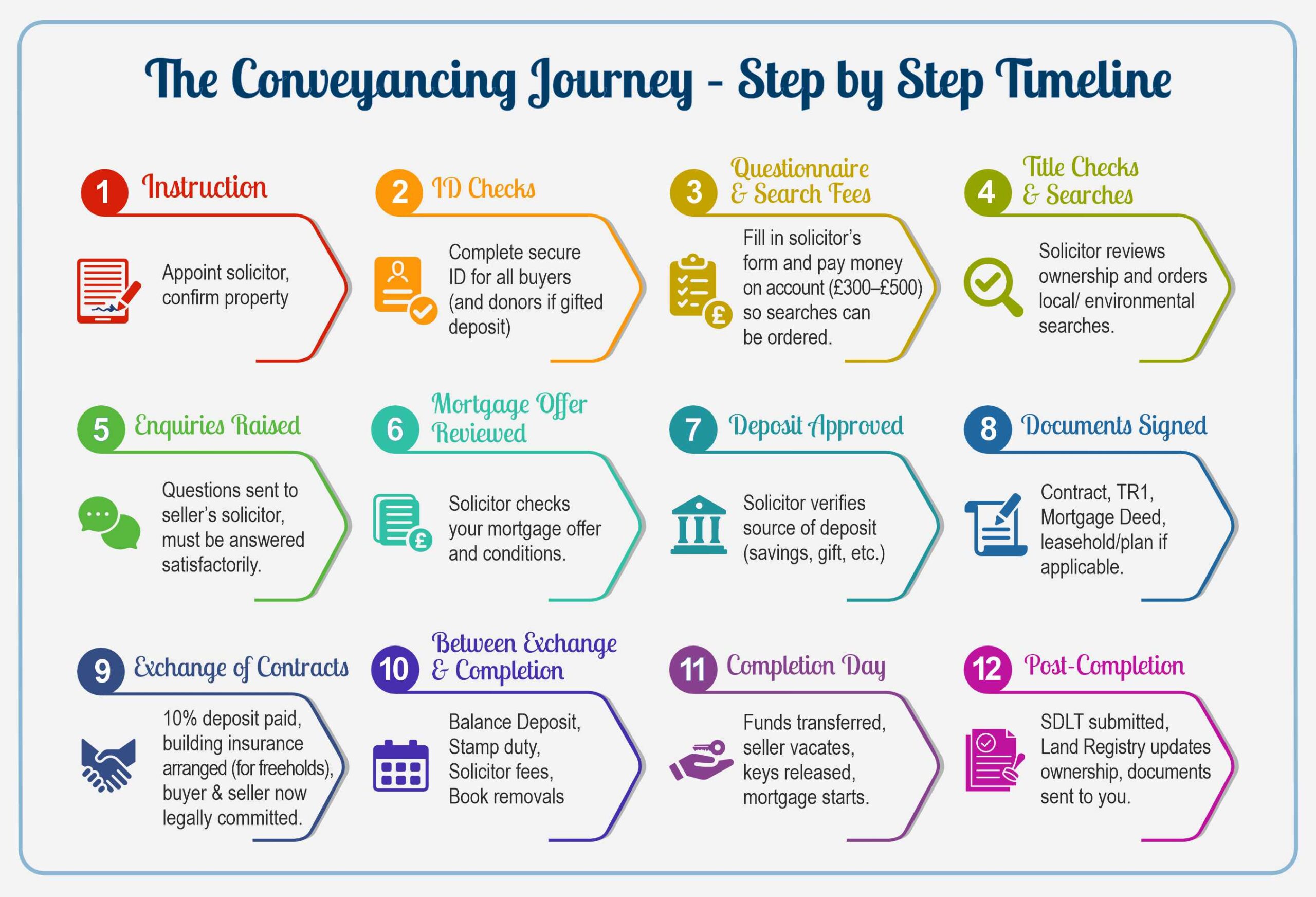

Starting the Conveyancing Process

Your solicitor can only begin once a few essential steps are complete.

From you

- Formal instruction: You confirm in writing that you want them to act for you, providing details such as property address, agreed price, and the names of all buyers. Once this is received, the solicitor opens a new file for your transaction.

- ID checks: Every buyer must complete ID checks. Increasingly, this is done through secure apps rather than just copies of passport and utility bills. If you are receiving a gifted deposit, the donor’s ID is also required.

- Client questionnaire: This detailed form collects information such as your National Insurance number, employment, buyer status (first-time buyer, home mover, additional properties), property details, bank account details for refunds and balances, and the source of your deposit. Many firms now collect this through an online portal.

- Money on account: Typically £300 to £500, used to pay for searches and other disbursements on your behalf. This is not an extra fee; it is drawn against actual costs.

From the agent and seller

- Memorandum of Sale: Provided by the estate agent, this confirms the deal, agreed conditions, and the details of both solicitors. It is the document that connects the buyer’s and seller’s solicitors.

- Draft contract pack: Sent by the seller’s solicitor to your solicitor. It includes the draft contract, title documents, Property Information Form, Fixtures and Fittings Form, and any relevant leasehold information if the property is not freehold.

Your solicitor can properly begin the conveyancing only once all of the above are in place.

Documents You Will Need to Sign

Before exchange, your solicitor will send you a set of documents to sign.

- Contract: Signed by all buyers confirming you agree to the purchase. Usually, this does not need to be witnessed.

- Transfer (TR1): This Land Registry document transfers ownership from seller to buyer. It must be witnessed by an independent adult. The witness:

- Cannot be related to you

- Cannot live at the same address

- Must be over 18

- Can witness for both buyers, but must sign against each name separately.

- Mortgage Deed: Gives your lender a legal charge over the property. Must also be signed and witnessed under the same rules.

- Leasehold forms and plan acknowledgement: If buying leasehold, you may be asked to sign to confirm your understanding of the property boundaries. Some solicitors also require a signature on the plan documents to confirm you know exactly which property within a development is being purchased.

We can witness signatures in our office if needed.

Your solicitor will also request the deposit for exchange at this point. Usually this is 10 percent of the purchase price, but alternative arrangements can sometimes be agreed.

Paying Your Solicitor Safely

Large sums are transferred during conveyancing, which unfortunately attracts fraud attempts. Always follow best practice:

- Verify bank details securely: Solicitors do not change bank details mid-transaction. Treat any message claiming otherwise as suspicious and phone the firm using a verified number.

- Use telegraphic transfer: Online banking often has daily limits. Telegraphic transfers carry a fee but are faster and safer for large amounts.

- Funds must come from your account: Solicitors will only accept funds from the buyer’s own account.

- Gifts from family should be paid into your account first.

- If using business funds, transfer them to your personal account before sending to your solicitor.

Keep transfers to as few payments as possible and always confirm receipt.

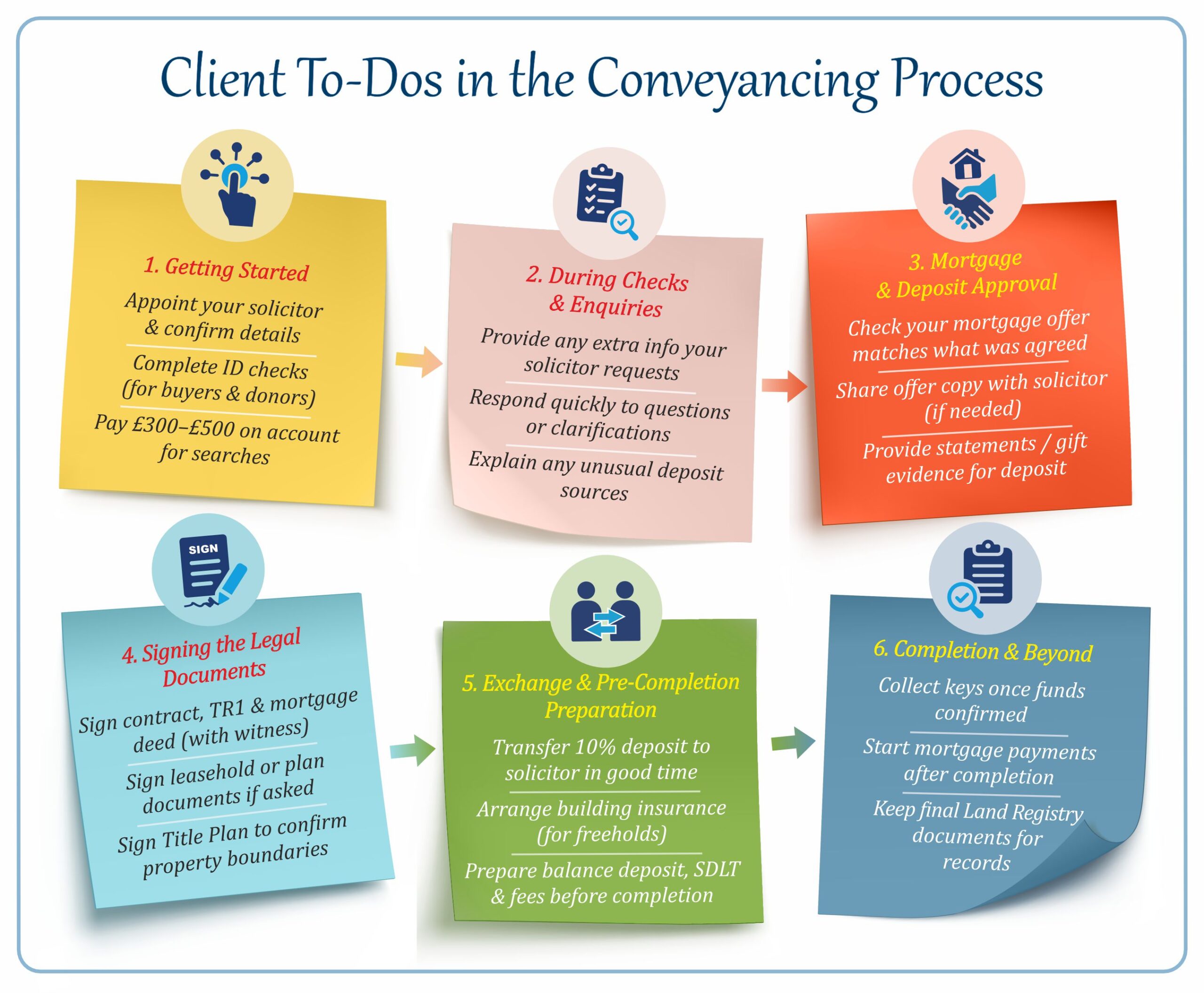

Buyer’s Checklist

- Instruct solicitor, provide full details, and complete ID checks.

- Return the client questionnaire promptly.

- Pay money on account to enable searches.

- Gather deposit evidence (including gift paperwork).

- Look out for document packs to sign and arrange a proper witness.

- Be ready to pay the 10 percent deposit at exchange.

- Plan for the balance deposit, SDLT, and fees at completion.

- Coordinate exchange and completion dates through your estate agent.

- Verify solicitor bank details and plan how you’ll transfer funds.

- Book removals once the completion date is fixed.