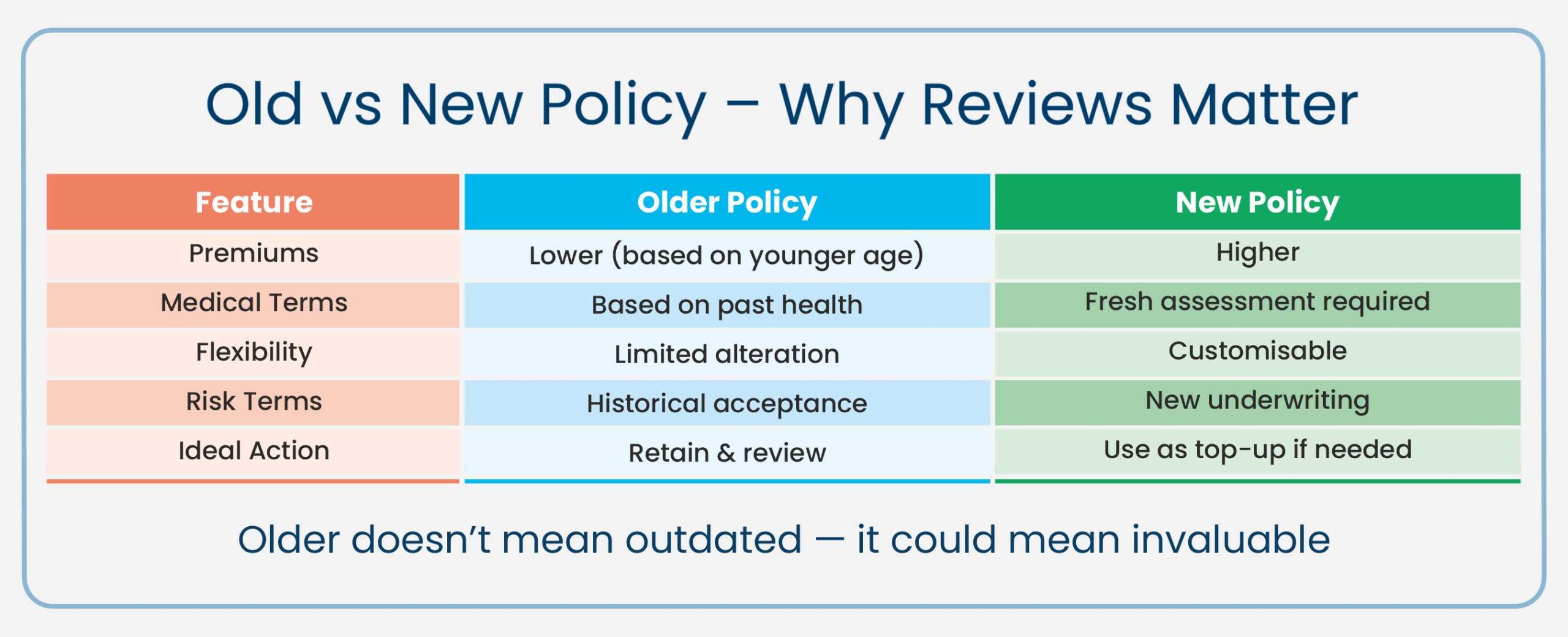

Older life insurance plans can often be genuine hidden gems.

Premiums are based on your age and health at the time you apply, which means policies taken out years ago often benefit from significantly lower, locked-in premiums and medical terms that may no longer be available today.

Before cancelling, altering, or replacing an existing policy, it is essential to seek professional advice. At Nachu Finance, we review older policies with care to ensure they remain relevant to your current needs, and we rarely recommend cancelling them unless there is a clear and meaningful benefit.

Because premiums rise sharply with age, older plans can offer outstanding long-term value compared to arranging cover later in life. Our premium comparison chart by age clearly shows how starting early keeps costs lower for the entire duration of the policy — you can view it Don’t Just Buy a Home-Protect It Too for a clearer picture.

Life evolves — so should your insurance.

Events such as marriage, buying a new home, having children, or changes in employment (for instance, moving from employed to self-employed) all affect your protection needs.

A periodic review helps you check whether:

- The level of cover matches your mortgage balance and family needs.

- Your term still aligns with your working years.

- Any employer benefits or other cover overlap with your personal policies.

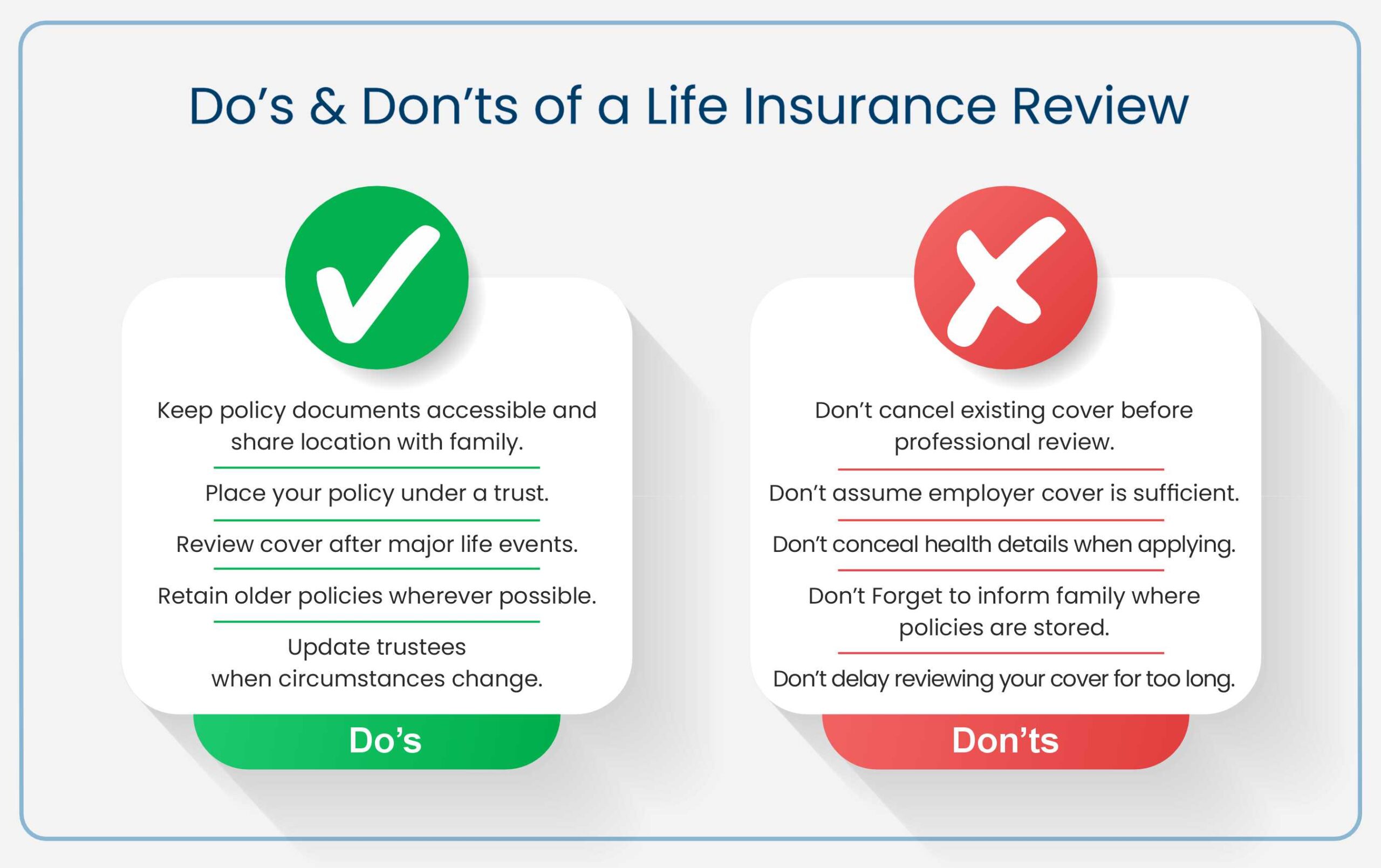

At Nachu Finance, we appreciate that older policies can hold immense value.

When we review your existing cover, we:

- Check if it remains suitable for your current family and financial circumstances.

- Help optimise it — including setting up or updating the trust.

- Securely store copies of your policies in your client file, so your family can easily access them in the event of a claim.

- Review both policies arranged by us and those you arranged elsewhere.

Even if no changes are needed, the reassurance that your policy is still fit for purpose is a valuable outcome in itself.