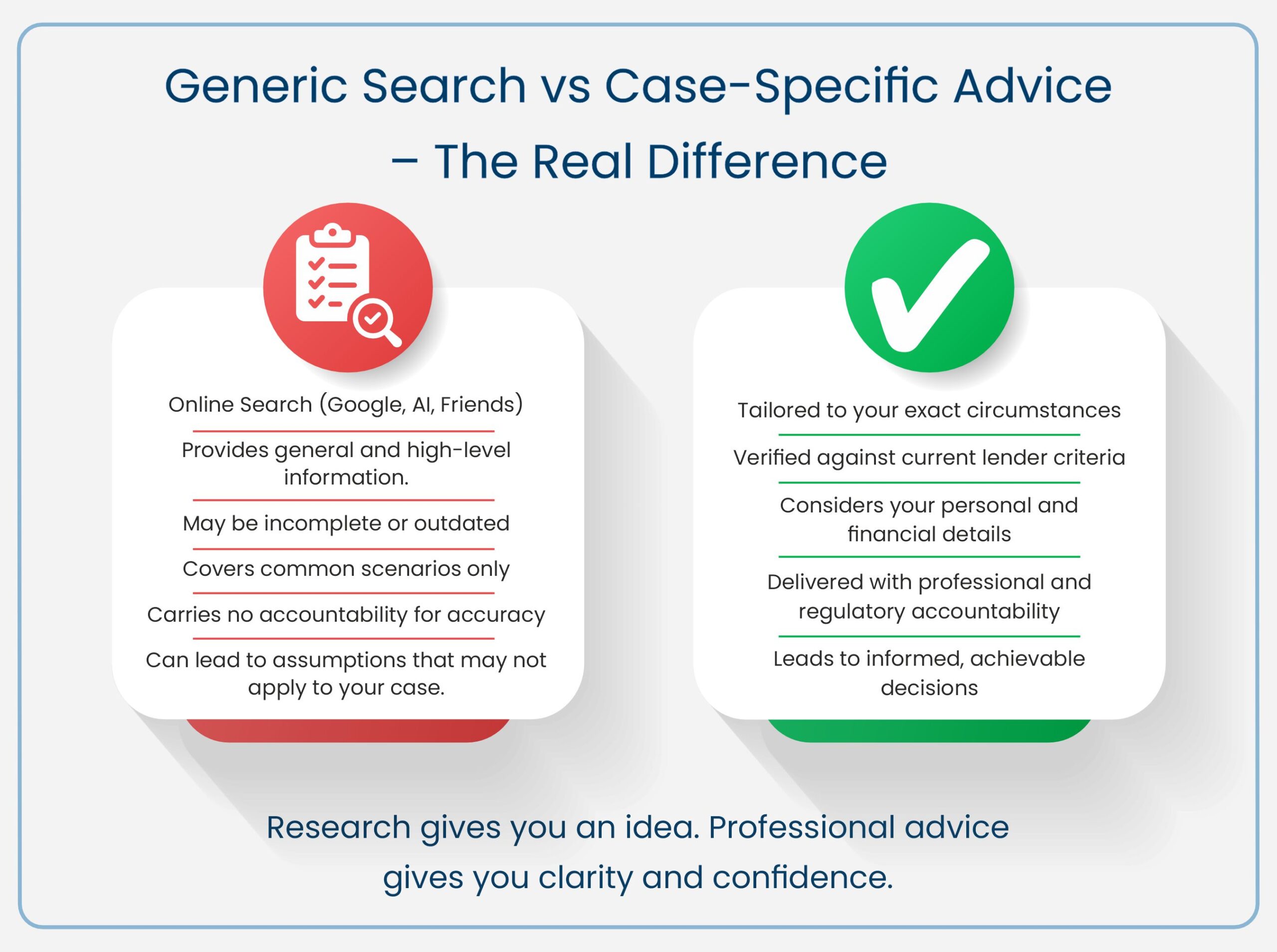

The Limits of Generic Information

The information found through a Google search or a general discussion with friends is, by nature, generic.

It does not take into account:

- Your income type or employment structure.

- The property’s ownership model or intended use.

- The lender’s current criteria.

- Your residency or credit profile.

Mortgage lending, taxation, and property law all have layers of detail that differ from one case to another. What works well for one individual may not be suitable or even possible for another.