Testmonials

Enquiry Form

Get in Touch with Us for Personalized Finance Assistance

Stamp Duty for Home Movers: How It Works and What to Consider

You’ve found your next home. You’ve accepted an offer on your current one. Then someone mentions stamp duty — and suddenly there’s a number on the table that nobody warned you about.

For most people moving home, stamp duty is straightforward. But miss one detail — the wrong property sold, a deadline not met, or an assumption about the rules — and the cost can run into tens of thousands of pounds.

This guide explains how stamp duty works for home movers, what qualifies you, how timing affects what you pay, and how refunds apply in practice.

Are You a Home Mover? What That Actually Means for Stamp Duty

Stamp duty broadly applies to buyers in three ways: first-time buyers (who may receive relief), home movers (standard rates), and additional property buyers (who pay a surcharge).

If you’re moving from one home to another, you would expect to fall into the home mover category. However, that classification is not automatic.

To qualify as a home mover, you must sell your current main residence and replace it with a new one. Simply selling any property you own is not enough.

If you’d like a broader overview of how stamp duty applies across all buyer types, you can read our detailed guide on stamp duty explained — the three buyer categories.

The property you sell must be your actual main home — not a buy-to-let, second home, or investment property. However, in practice, determining what counts as a “main residence” is not always straightforward.

If you live in only one property, that will generally be your main residence. Where more than one property is involved, HMRC looks at the overall facts and circumstances to determine which one qualifies. This is not something you can nominate — it is based on objective evidence.

Factors that may be considered include where your family lives, where children go to school, your place of work, where you are registered to vote, and which address is used for day-to-day living such as correspondence, council tax, and healthcare registration. No single factor is decisive — the overall picture is what matters.

It is also important to note that simply occupying a property for a short period does not automatically make it your main residence. There needs to be a degree of permanence and expectation of continuity.

When replacing a main residence, HMRC applies two tests. The property being sold must genuinely have been your main residence at some point, and the property being purchased must be intended to become your main residence at the time of purchase, even if occupation happens shortly afterwards.

As these rules are based on HMRC guidance and applied to the specific facts of each case, determining what qualifies as a main residence can become complex, particularly where multiple properties or changing living arrangements are involved. For full detail, you can refer directly to HMRC’s guidance on this topic:

https://www.gov.uk/hmrc-internal-manuals/stamp-duty-land-tax-manual/sdltm09812

Where there is any uncertainty, it is advisable to seek guidance from a qualified tax professional to ensure the correct treatment.

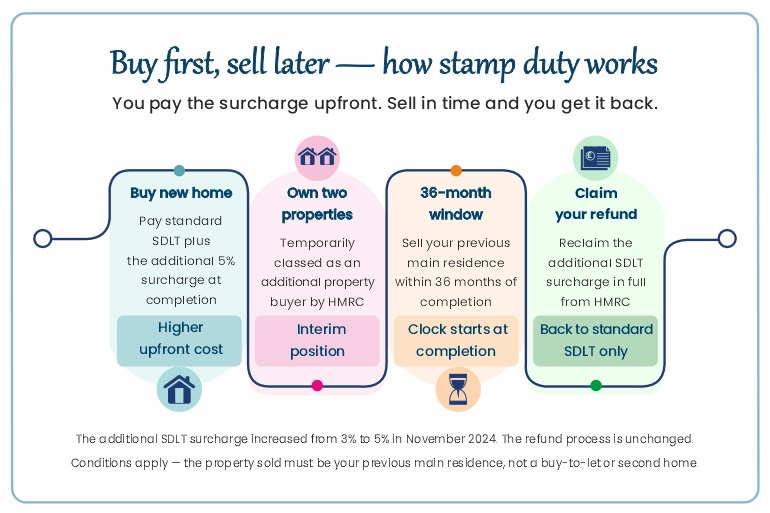

Understanding the 36-Month Rule

The 36-month rule is central to how stamp duty works for home movers when your sale and purchase do not happen at the same time. If you buy first, you must sell your previous main residence within 36 months of completing on your new purchase — the clock starts at completion, not at exchange or when you move in. If you sell first and then buy, there is no equivalent 36-month requirement. The rule only applies in one direction.

The Three Scenarios: Buy and Sell Timing Matters

In practice, there are three possible ways a home move can happen, and stamp duty treatment depends on which scenario applies.

If your sale and purchase complete at the same time — typically as part of a property chain — you are treated as a home mover immediately, meaning only standard stamp duty rates apply and no surcharge is payable. However, being in a chain can introduce practical challenges around timing and dependency on other transactions. This is explored further in our article on options for breaking a property chain.

If you sell your current home before buying your next one, the position remains straightforward from a stamp duty perspective. You will be treated as a home mover at the point of purchase, with no surcharge payable. However, this may involve additional practical considerations such as temporary accommodation or multiple moves.

If you buy your new home before selling your existing one, you will temporarily own two properties. In this situation, HMRC treats you as an additional property buyer, meaning you will pay standard stamp duty plus the additional surcharge, which is currently 5% (increased from 3% in November 2024). You will then have 36 months to sell your previous main residence, after which you can claim a refund of the surcharge, provided all conditions are met.

Worked Examples: How This Works in Practice

To bring this to life, the following two case studies illustrate how stamp duty applies in practice where the new home is purchased before the existing one is sold. In both scenarios, the additional stamp duty is paid upfront and later reclaimed once the previous main residence is disposed of within the permitted timeframe.

Case Study 1: Typical Home Mover (Simple Scenario)

Alex and Olivia (names changed) were living in a two-bedroom flat and decided to move to a three-bedroom house. The new property was purchased for £465,000 in September 2025, while their previous flat, valued at £240,000, was sold five months later in February 2026.

At the point of purchase, they owned two properties and therefore paid both the standard stamp duty and the additional surcharge. The standard stamp duty on the purchase was £13,250, and they also paid an additional £23,250, representing 5% of the £465,000 purchase price.

Once their previous main residence was sold within the required timeframe, they successfully claimed back the £23,250 additional stamp duty from HMRC. This meant their final net stamp duty cost remained at £13,250.

This example illustrates a straightforward buy-first scenario where the additional stamp duty is a temporary cost. Provided the timelines are met and the correct property is sold, the final outcome reflects standard home mover treatment.

Case Study 2: Higher Value and More Complex Scenario

Steve and Priya (names changed) owned multiple properties, including their main residence, and chose to purchase a new home valued at £2,000,000 in 2022 before selling their existing one. At the time, they paid standard stamp duty of £153,750 along with an additional 3% surcharge of £60,000.

Following the purchase, they later transferred their former main residence into a limited company structure. For stamp duty purposes, this transfer was treated as a disposal, which meant the conditions for replacing their main residence were satisfied and the £60,000 surcharge was successfully reclaimed.

As explored further in our article on transferring property from personal name to a limited company, this type of approach can work in certain scenarios but requires careful planning. The key point is that stamp duty treatment is driven by ownership — not how the property is used.

Checklist: Getting It Right as a Home Mover

To ensure the correct stamp duty treatment, it is important to confirm which property qualifies as your main residence and to ensure that this is the property being sold. You should carefully track the 36-month timeline, keeping a clear record of both purchase and sale completion dates.

Where multiple properties are involved, understanding your ownership structure becomes particularly important. If a refund is due, it should be claimed promptly once the relevant transaction has completed. In more complex situations, including those involving company ownership or unclear residence status, seeking professional advice is strongly recommended.

The infographic below will provide an overview of the steps involved

Key Takeaways

You must replace your main residence, not simply sell any property you own. The timing of your transactions directly affects how stamp duty is applied, and the 36-month rule plays a critical role in determining whether a refund is available. Ownership — rather than usage — is what ultimately determines treatment. While many straightforward cases can be managed directly, more complex situations require careful planning and professional advice.

Important Disclaimer

This article is for informational purposes only and does not constitute tax advice. It is designed to explain how stamp duty works in practical scenarios and to share illustrative examples. You should always carry out your own due diligence and consult a qualified tax professional before proceeding with any property transaction.

Frequently Asked Questions

No. Stamp duty treatment is determined by ownership rather than usage. Whether the property is rented out, occupied by a family member, or left vacant does not affect eligibility. The key consideration is whether the property remains in your name.

In certain circumstances, yes. If the property is transferred from your personal name to a limited company, ownership moves to a separate legal entity, which can count as a disposal for stamp duty purposes and allow a refund to be claimed. However, this must be assessed carefully, as the company itself may incur stamp duty on acquisition. As discussed in our article on transferring property from personal name to a limited company, this strategy is not always appropriate and depends on the wider tax position.

If ownership of the property is transferred out of your name to a family member, this can be treated as a disposal for stamp duty purposes, meaning you may be able to claim a refund of the additional stamp duty paid. However, transferring property in this way brings wider tax and legal implications, including potential capital gains tax and inheritance tax considerations. It is important to take professional advice before proceeding.

Where multiple properties are owned, HMRC applies specific rules to determine which one qualifies as your main residence. This is not always straightforward, particularly where more than one property is used at different times. In such situations, referring to HMRC guidance and seeking professional advice is recommended to ensure the correct treatment.

About the Author

Sekkappan Alagu is the Founder of Nachu Finance Ltd, established in 2006. With an early career in journalism and publishing, he brings clarity and structured thinking to complex financial topics. Through the Nachu Finance Blog and Knowledge Hub, he shares insights drawn from nearly two decades of client advisory experience, helping readers make informed decisions and understand best practices in mortgages, protection and long-term financial planning.

Business Profile

Nachu Finance Ltd is a directly authorised FCA-regulated firm providing mortgage, insurance and estate planning advice to clients across the UK. The firm takes a holistic approach — considering protection, tax efficiency and long-term planning alongside property finance — maintaining high regulatory standards while keeping advice clear and easy to follow. To learn more about the firm's background and story, visit the About Nachu Finance page.

Continue Strengthening Your Financial Understanding