Testmonials

Enquiry Form

Get in Touch with Us for Personalized Finance Assistance

Explore Your Remortgage Options with Confidence

When you approach the end of your current mortgage deal, it’s the ideal time to review your mortgage in full. This isn’t just about finding a new rate — it’s a valuable opportunity to ensure your mortgage still aligns with your current circumstances and financial goals. Whether you’re looking to reduce costs, release equity, or make ownership changes, a remortgage could offer the flexibility you need.

Always Start with Your Current Lender

When a fixed or initial deal comes to an end, your existing lender should usually be the first port of call. Since they’ve already assessed your profile and the property, they may offer a new rate through what’s called a product transfer — a relatively simple process without the need for full underwriting or solicitor involvement.

Why consider your current lender first:

- No need for a fresh valuation in many cases

- No legal work or solicitors required

- Fewer documents and simplified process

- Often quicker to complete

We offer a dedicated Product Transfer Service to help you assess these offers and decide whether they’re competitive compared to what’s available across the market.

When a Remortgage Becomes the Better Option

There are many situations where sticking with your current lender may not serve your best interests, and a full remortgage to a new lender could be more beneficial — even if it involves slightly more effort.

Scenarios where a remortgage makes more sense:

- You need additional borrowing and your current lender’s further advance options aren’t suitable

- You want to reduce your loan significantly and your lender doesn’t support large overpayments or favourable terms for smaller balances

- Your lender’s new rates are not competitive and you could achieve notable savings with another provider

- Changes in ownership are needed — for example, adding or removing someone from the mortgage

- Your circumstances have improved and you may now qualify for better rates from mainstream lenders

- You own a property outright (unencumbered) and want to release equity through a mortgage.

- You are changing the use of the property — for example, switching from a buy-to-let to a residential mortgage (or vice versa) based on how you now plan to occupy or let the property.

- You want a longer mortgage term, and your current lender doesn’t offer flexibility — many lenders now allow terms up to age 75, helping keep monthly payments more affordable

While a remortgage involves a new mortgage application, credit and affordability checks, a valuation, and legal work via solicitors — it is still far less intensive than the home purchase process and can be well worth it for the right reasons.

Not All Lenders Are for Life

Some lenders position themselves as ‘lenders for life’, offering long-term competitive options and aiming to retain clients as their circumstances evolve. Others serve more as stepping stones — ideal at the time due to credit issues, unusual income structures, or non-standard properties.

If you originally chose your lender due to:

- Poor credit or recent financial issues

- Unusual deposit source or ownership structure

- A property that initially required renovation and is now in better condition.

- Being newly self-employed or having limited income history

…you may now be in a better position to move to a high street lender with better rates and long-term flexibility.

Planning Ownership Changes? Remortgage Is the Right Time

If you wish to add someone new to the mortgage (e.g. a partner) or remove an existing borrower (e.g. after separation), a remortgage is the ideal time to handle this. This process is known as a transfer of equity and will be handled by the solicitors as part of the remortgage legal work.

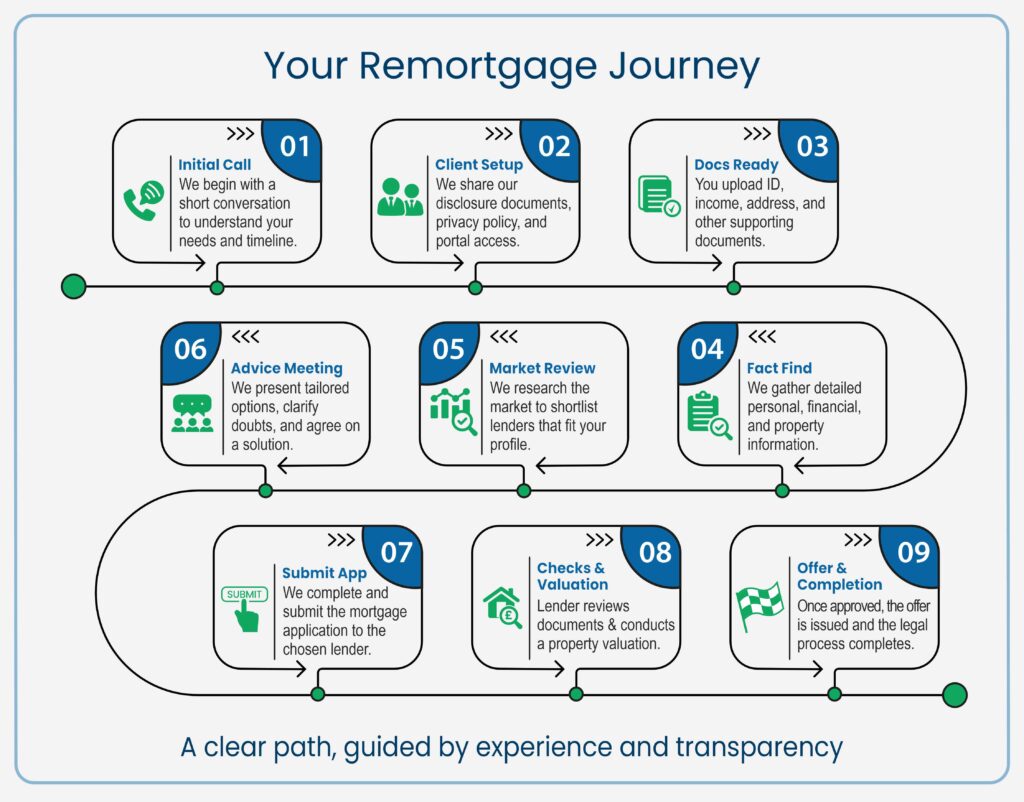

Remortgage Process Explained

Step-by-step process:

Your Remortgage Journey – What Happens Behind the Scenes

We’ve outlined the core steps in the infographic above — but here’s a closer look at what happens at each stage, and how we support you throughout the process:

Understanding Your Goals

It all starts with a short, informal conversation to understand where you are in your mortgage journey, what you’re hoping to achieve, and what timelines we’re working with.

Setting Things Up

Once we’ve agreed to proceed, we take care of all regulatory requirements and provide you with access to our secure client portal — where you can upload documents and track progress with ease.

Gathering the Right Information

We’ll request a tailored list of documents such as ID, proof of address, income records, and anything relevant to your property or mortgage. This helps us build a complete picture.

Going Beyond the Basics

Through a structured fact-find, we explore details like your family setup, address and employment history, financial commitments, and how you prefer to manage money. This ensures our advice is fully aligned with your circumstances.

Researching the Market

With your information in hand, we explore suitable lenders across the market. It’s not just about finding the best rate — we also consider lender policies, term flexibility, and long-term suitability.

Presenting Your Options

Once our research is complete, we arrange a review meeting — either in person or online — to talk you through your options, answer questions, and finalise the way forward.

Submitting the Application

We then prepare and submit your mortgage application, ensuring everything is packaged clearly and correctly to minimise delays or queries from the lender.

Valuation and Assessment

The lender will review your documents, carry out affordability checks, and arrange for the property to be valued before making a final decision.

Final Offer and Completion

If all goes smoothly, you’ll receive a formal mortgage offer. Legal work follows — often through a solicitor appointed by the lender — and we stay in touch with you and all parties until completion.

Common Client Scenarios

Over the years, we’ve helped clients remortgage for a wide range of reasons — not just because their rate was ending. Here are some of the more common situations where a remortgage was the right step forward:

🤵 “My credit score has improved — can I now get better rates?”

🤵 “My income has increased and stabilised since the previous mortgage — can I switch to a better lender?”

🤵 “My current lender’s rates seem out of sync with the market.”

🤵 “I need to alter the term of my mortgage, but it’s proving difficult with my existing lender.”

🤵 “I want to consolidate some debts while remortgaging.”

🤵 “I’ve come into savings and want to reduce the mortgage term or balance.”

🤵 “I’m looking to raise additional funds to invest in another property.”

🤵 “We’re planning home improvements and need extra borrowing.”

🤵 “I need to add my partner to the mortgage.”

🤵 “I’d like a longer mortgage term — more lenders now offer terms up to age 75 to help with affordability.”

Early Repayment Charges and Timing Strategy

One of the most overlooked aspects of remortgaging is understanding when to act. Time it wrong, and you could either overpay or miss the window to secure a better deal.

Important timing points to consider:

- Don’t wait until your deal ends — begin reviewing options 4 to 6 months in advance

- Avoid rolling onto a standard variable rate (SVR), which is usually higher and costlier

- Align completion with the expiry of your early repayment charge (ERC) to avoid unnecessary penalties

Getting this timing right is crucial. At Nachu Finance, we’ll help you navigate it smoothly.

Fees and Costs to Expect

Remortgaging may be simpler than buying a new home, but it still involves some costs. Understanding what to expect early on helps prevent surprises later.

Typical costs may include:

- Lender fees, such as arrangement or valuation fees (some lenders waive these)

- Legal fees, often covered by the lender or refunded via cashback

- Adviser fees, where applicable

At Nachu Finance, we believe cost transparency is just as important as cost-efficiency. While generalised figures can mislead, we provide a tailored cost breakdown for each solution, discussing not just the fees, but the true net benefit after considering both direct and indirect costs. Our advice is always bespoke — not one-size-fits-all.

Why Choose Nachu Finance for Your Remortgage?

Remortgaging is more than just switching to a new rate. It’s an opportunity to make strategic decisions that can shape your long-term financial stability. Here’s why clients across the UK trust us for this important step:

- Whole-of-market advice — we’re not tied to any one lender, giving you access to the full range of options

- Almost two decades of experience — advising and arranging mortgages since 2006

- Holistic financial advice — we look beyond the mortgage, offering guidance on insurance and estate planning to help protect your family and build a secure future

- Expertise in both straightforward and complex cases — whether you’re adding a partner, releasing equity, or restructuring the term

- Skilled deal structuring — we help optimise loan amount, term, repayment method, and ownership setup

- Client-first service — tech-savvy, flexible, and available through secure portals, Zoom, and WhatsApp

- Multilingual support — Tamil-speaking advisers available for clients who prefer advice in their mother tongue

- Trusted by returning clients — many of our clients come back to us for future needs and confidently refer their friends and family

Our Transparency Process

Thorough for a Reason

At Nachu Finance, we believe in full transparency from the start.

We may request additional documents to ensure every aspect of your application is accurately assessed — not to complicate the process, but to ensure every detail aligns with lender requirements, legal regulations, and most importantly, your long-term interest. Our experience has shown that thorough preparation upfront prevents delays and surprises later.

This extra effort reflects our commitment to getting it right the first time, and to giving you peace of mind throughout the remortgage journey.

Smart Remortgaging Starts Here

Whether you’re nearing the end of your fixed rate, need to release funds, or are looking to restructure ownership, we’re here to help.

Contact us and take your first step to joining the several happy Nachu Finance clients.

As experienced, transparent, whole-of-market advisers with a flexible, client-focused approach, we’ll help you make the most informed and beneficial remortgage decision possible.