Testmonials

Enquiry Form

Get in Touch with Us for Personalized Finance Assistance

Even with the most carefully planned estate strategies, some Inheritance Tax (IHT) liabilities may still remain. Life insurance, when used strategically, can play a vital role in ensuring your family receives the full value of your assets-without the stress of forced sales, bridging loans, or large upfront tax payments. When tax can’t be fully mitigated through reliefs or asset transfers, a well-structured life policy can provide the funds needed to pay the IHT efficiently and preserve your legacy as intended.

What Is Inheritance Tax?

Inheritance Tax (IHT) is a tax on the estate-property, money, and possessions-of someone who has passed away. Each individual is entitled to a standard tax-free allowance of £325,000, known as the Nil Rate Band (NRB). Anything above this may be taxed at 40%.

In addition, some individuals may qualify for a further allowance of up to £175,000 under the Residential Nil Rate Band (RNRB), subject to certain conditions-such as who inherits the property and the total value of the estate.

These allowances apply per person, meaning a couple could potentially pass on between £650,000 and £1 million tax-free, depending on their circumstances.

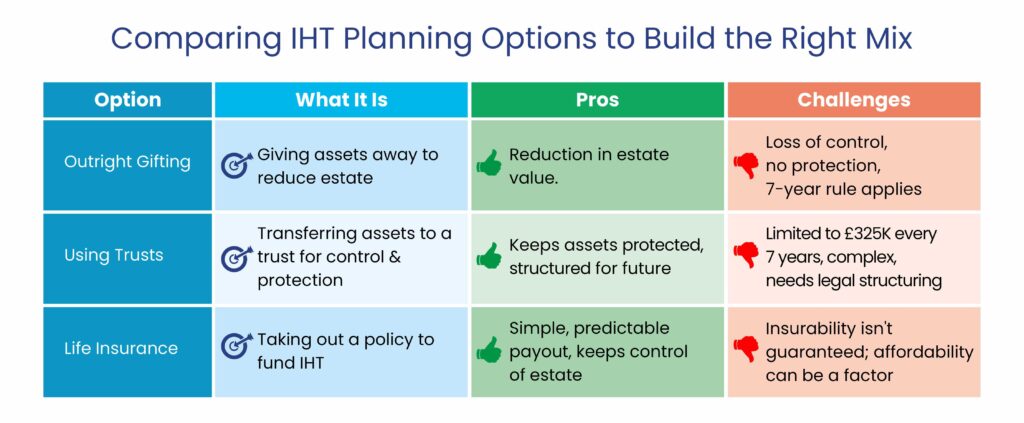

Can’t Give Away Too Early

While the concerns around IHT are valid and planning ahead is essential, it’s equally important not to compromise your own financial security. As the wealth creator, you’ll want continued access to both the capital and the income it generates during your lifetime.

Transferring assets to the next generation too early-solely to reduce future IHT-can be short-sighted and may result in financial strain later in life. A rushed approach to giving away assets without regard to long-term needs can lead to poor financial outcomes, potentially undermining the very goals of your estate planning.

Restrictions on How Much Can Be Given Away Efficiently

Although there’s technically no cap on how much you can gift to your children or others, doing so without careful planning carries significant risks. Outright transfers offer no protection from events such as divorce, bankruptcy, or care costs, nor do they allow you to control how those assets are managed or used by the recipient.

Using a trust structure is often a more prudent approach. By placing assets into a trust for the benefit of your children, you gain both greater control and stronger protection. However, this method has its limitations: you can transfer up to £325,000 into a trust every seven years without triggering additional tax consequences. If your aim is to transfer wealth in a tax-efficient and controlled manner, these allowances must be carefully considered and strategically used.

IHT Is Payable Upfront

One of the key challenges with Inheritance Tax is that it becomes payable shortly after death-typically before beneficiaries have full access to the estate. This can create liquidity issues, especially when much of the estate is tied up in property or other illiquid assets.

Life Insurance Can Avoid the Need to Dispose of Assets

A life insurance payout can give your beneficiaries the flexibility to retain inherited assets-such as a family home or investment property-rather than being forced to sell them under pressure to meet IHT obligations. In some cases, families may even be required to take a bridging loan to cover the tax bill before gaining legal ownership of the estate. A policy written in trust avoids this scenario and preserves the legacy in full.

Is This Relevant to You?

Are you concerned your family might have to sell property or take out loans to pay the tax?

Do you want to pass on your assets in the most efficient way possible?

If yes, then incorporating life insurance into your estate planning could be one of the most impactful decisions you make.

Rightly Planned Life Insurance Can Help Pay IHT

A well-structured life insurance policy, written in trust, can be a highly effective way to ensure that the necessary funds are available when the IHT bill is due. Rather than forcing the family to sell assets or take loans, the policy provides a timely and tax-free payout that can be used specifically to settle the inheritance tax liability.

Read more on why placing your life insurance in trust is a smart move →

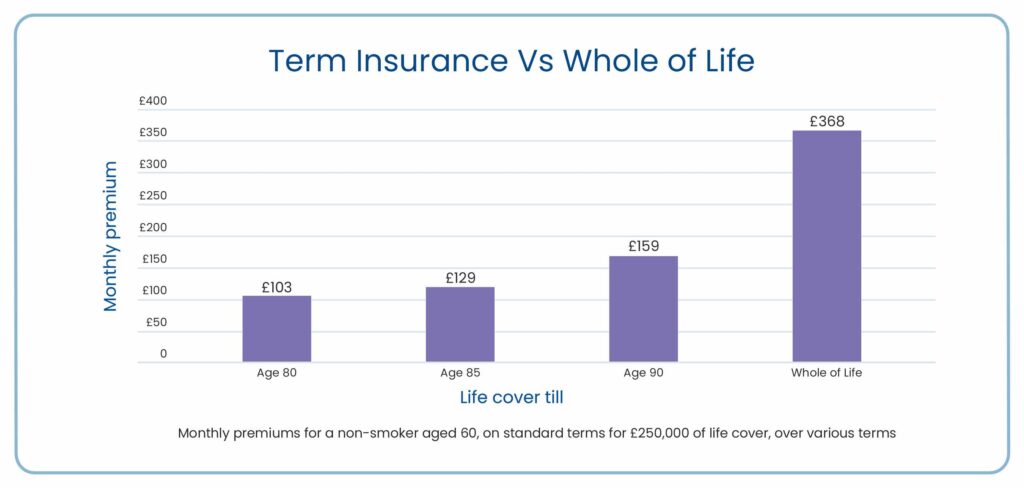

Whole of Life vs Term Insurance

Whole of Life (WoL) policies offer the ideal structure for covering IHT-guaranteed payout whenever the life assured passes away. However, over the years, premiums for such policies have increased significantly.

While WoL should certainly be considered, many clients find that longer-term insurance policies-lasting until age 80, 85, or even 90-can offer a cost-effective alternative. These still provide valuable cover over the likely window of liability and often come with far more affordable premiums.

Who Pays for the Policy?

Typically, the person undertaking the IHT planning pays the policy premiums-but this doesn’t have to be the only option. Involving the next generation in this planning can be practical and even welcomed. After all, the purpose of this insurance is to ensure they receive the legacy you’ve built with minimal tax erosion.

In our experience, many adult children are open to contributing to premiums when they understand it ultimately safeguards the value of the inheritance they will receive.

Insurability Is Not Guaranteed

It’s important to recognise that not everyone will be eligible for life insurance to support their Inheritance Tax (IHT) planning. Age, health conditions, and medical history all play a role in whether insurers are willing to offer cover-and on what terms.

If you are in a position where life insurance is available to you, that in itself is a significant advantage. Being insurable is a blessing-not something to take for granted-and it opens up a powerful option to protect your legacy in a tax-efficient way.

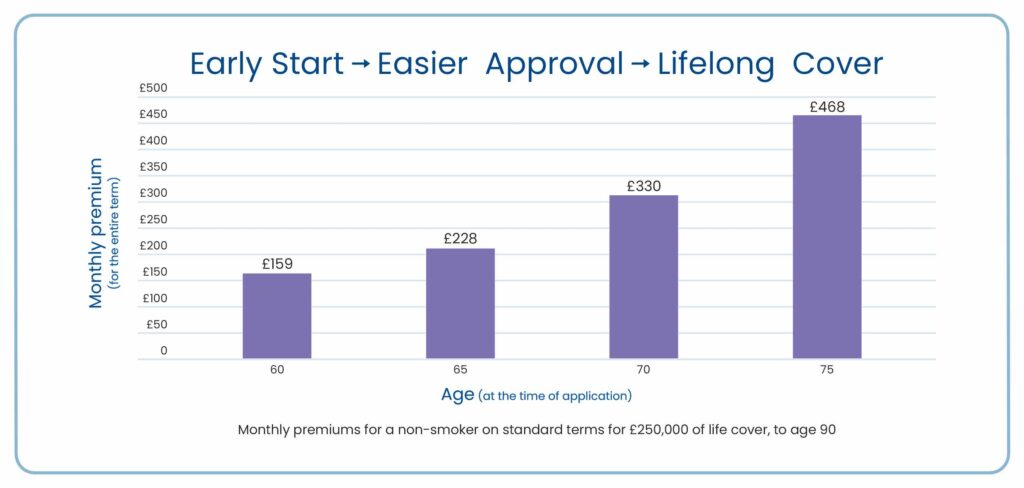

Starting Early is Beneficial

Just like with life insurance in the context of a mortgage, the earlier you begin planning for IHT, the better your options. Younger applicants benefit from lower premiums, higher acceptance rates, and more flexibility in policy design.

Integrated Advice for Better Estate Planning Outcomes

At Nachu Finance, our ability to advise on both estate planning and life insurance means we can offer a joined-up strategy. Whether it’s considering the use of trusts, reviewing your asset structure, or arranging life insurance tailored to your estate’s needs, our holistic approach ensures that all elements work together to meet your goals.

Real Life Case Studies

While we often include more than one case study, the following example offers a wide-ranging look at the key considerations involved in life insurance and inheritance tax planning-making it an ideal standalone story to illustrate the process and value of good advice.

Please note: names and certain details have been adjusted to maintain client confidentiality.

Case Study: Life Cover Strategy for a Professional Landlord

Aiswarya, a professional landlord with multiple buy-to-let properties and a residential home, has been a client of Nachu Finance since 2010. As a widow with one daughter and no other source of income, her rental income is essential for her day-to-day living Naturally, she was cautious about giving up control of her portfolio too early-especially since transferring all of her buy-to-let properties into a trust would not be straightforward or tax-efficient.

Understandably, she was also concerned about passing the properties directly to her daughter, who was unmarried at the time, and instead preferred to plan for the future through Trusts when the time is right.

In 2018, based on our advice, Aiswarya took out a life insurance policy of £250,000 over a 30-year term, accepted on standard terms at a monthly premium of £170. While we presented options for higher cover, she chose this level as a balance between protection and affordability.

When we revisited her planning in 2025, her daughter was involved in the review and could clearly appreciate the benefit of having life insurance in place to help cover potential Inheritance Tax liabilities. They agreed it would be sensible to increase the cover. However, at 67 years old, Aiswarya was now being quoted £240 per month for an additional £250,000 of cover until age 90. After reviewing a matrix of options we provided, she applied for £200,000 of additional cover-expected to cost £197 per month.

Due to new health disclosures in 2025, the best terms available included a 50% loading on the premium. After further review, Aiswarya decided to proceed with £150,000 of additional cover at £233 per month.

She now holds life insurance totalling £400,000, in place until her 90th birthday. Both she and her daughter feel confident that this cover will significantly help meet any future IHT liability. This case highlights two important lessons: the value of starting early, and the benefit of involving future beneficiaries in the planning process-ensuring the solutions put in place are understood, appreciated, and aligned with the family’s long-term goals.

How Nachu Finance Can Help

At Nachu Finance, we bring decades of experience in financial services along with a deep understanding of estate planning to help you make informed, confident decisions.

Our approach goes beyond simply arranging a life insurance policy-we take the time to understand your broader goals, family needs, and any medical or personal circumstances that may affect the options available. We use our whole-of-market access to research and identify the most suitable providers, including those more likely to accept specific health conditions, ensuring no time is wasted applying to unsuitable insurers.

We’re committed to offering a variety of solutions tailored to your requirements, backed by transparent advice and regular reviews to ensure your cover stays relevant as circumstances change. And when it comes to making a decision, we’re here to guide-not to push-so you can choose with clarity and confidence.

Our Transparency Promise

Will not push or over promise

At Nachu Finance, we believe clear, honest advice is the foundation of good estate planning-especially when it comes to life insurance and Inheritance Tax (IHT).

We’ll always be upfront about

- whether life insurance is a realistic option for you

- the likely premiums and

- any potential health-related limitations that may apply

We won’t overpromise or push unsuitable products. If life cover is not the right solution based on your circumstances, we’ll tell you that-and help you explore alternatives where appropriate.

This isn’t about selling policies. It’s about protecting your legacy with advice that puts your best interests first.

Let’s Secure Your Legacy - Get in Touch

Inheritance Tax planning isn’t just about numbers-it’s about securing what you’ve worked hard to build and passing it on efficiently.

Whether you’re exploring your options, want to check your insurability, or simply need a second opinion-we’re here to help.

✅ Expertise in both estate planning and life insurance

✅ Whole-of-market access to find the right providers

✅ Understanding of medical underwriting and trust arrangements

✅ Advice tailored to your family’s unique situation

✅ Clear, honest guidance-never pressure or hard selling

Contact Nachu Finance today and take the next step in protecting your family’s future.