Testmonials

Enquiry Form

Get in Touch with Us for Personalized Finance Assistance

Property Chain Breaking Options

- Date Published :

Practical ways to move home without being held back by the chain

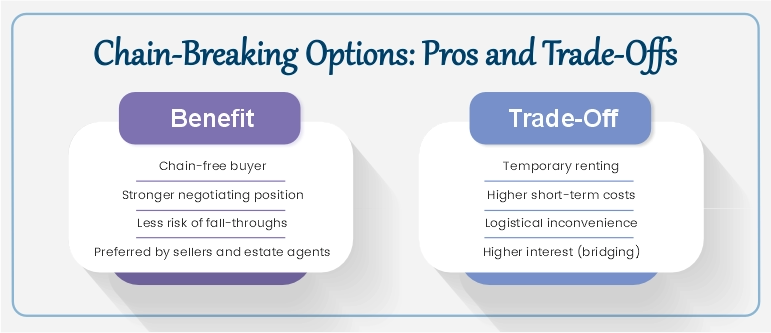

Buying a property when you already own one brings an extra layer of complexity. Unlike first-time buyers, home movers are often part of a property chain, relying on their own sale while also depending on the seller of the property they wish to buy.

In slower or uncertain markets, chains are more likely to collapse. Buyers may lose confidence, sellers may become impatient, and transactions can fall through even late in the process. Being in a chain can therefore weaken your negotiating position and limit your choice of properties.

This article looks at the main options available to home movers who want to reduce or remove the risk of being held back by a chain, along with the practical trade-offs involved in each approach.

01. Let-to-Buy (Keep the Current Property)

If you are happy to retain your existing home and let it out, a let-to-buy arrangement can remove the need to sell before buying.

How it works

- Your current residential property is converted to a buy-to-let mortgage.

- Rental income is used to support the new mortgage.

- Where affordability allows, equity may be released from the current property towards the new purchase.

- If no equity is required, it can be a straightforward transfer of the existing mortgage to a buy-to-let basis.

Key advantage

- You are not reliant on selling, so you are no longer in a chain.

Key considerations

- Not all properties or borrowers are suitable.

- Rental stress tests and tax implications need careful assessment.

- This works best where long-term landlord ownership is acceptable.

02. Non-Simultaneous Completion (Buy First, Sell Later)

If your new purchase is not dependent on releasing equity from your current home, you may be able to buy first and sell later.

How it works

- You complete on the new home using savings, investments, or other funds.

- You move into the new property.

- The existing property is sold afterwards.

Key advantage

- You become a chain-free buyer, significantly strengthening your position with sellers.

Key limitation

- You cannot access equity from the existing property until it is sold.

- This option is only viable for buyers with sufficient independent funds.

03. Sell First, Then Rent Temporarily

For many buyers who do need the equity, selling first and moving into rented accommodation can be an effective chain-breaking strategy.

How it works

- You sell your current home and release the equity.

- You move into short-term rented accommodation.

- You then buy your next home as a chain-free buyer.

Key advantage

- Maximum negotiating power when buying.

- No dependency on other parties.

Key drawback

- Logistical inconvenience of two moves.

- Temporary disruption and rental costs.

04. Bridging Finance

Where timing is the issue and you still need funds from your current property, bridging finance may be an option.

How it works

- A short-term loan allows you to complete the new purchase before selling.

- You move into the new property immediately.

- Once the existing property sells, the bridge is repaid.

Key advantage

- Avoids renting and avoids chain dependency.

Key drawback

- More expensive than standard mortgages.

- Requires a clear exit strategy and careful risk management.

05. Part Exchange with a New-Build Developer

If you are buying a new-build property, some developers offer part exchange.

How it works

- The developer buys your existing property.

- Its value is offset against the purchase price of the new home.

- The developer takes on the responsibility of selling your old property.

Key advantage

- Smooth, chain-free process.

- Reduced risk of delays or fall-throughs.

Key consideration

- Valuation is set by the developer, which may limit negotiation.

- Only suitable where the offered price aligns with your expectations.

Real-Life Scenarios (Illustrative Examples)

Below are three real-life scenarios illustrating how different strategies were used to break a property chain, helping you understand how the most suitable option will depend on your individual circumstances.

A couple struggled for months to sell their flat while trying to buy a house. Being in a chain was repeatedly cited as a concern by sellers. They decided to sell first, rent temporarily, and then buy.

Outcome:

- Chain removed

- Better negotiating position

- Successful purchase at the right price

Compromise: temporary rental and an extra move.

Another couple upgraded to a larger family home using savings and investments rather than relying on their existing sale. They paid the additional property stamp duty upfront and sold their original home later, reclaiming the extra stamp duty once the sale completed.

Outcome:

- No chain

- No logistical disruption

- Sale completed at full market value

Limitation: required sufficient upfront capital.

In a buoyant market, a buyer and seller were both comfortable proceeding despite the chain. The transaction took longer but completed without price compromise.

Outcome:

- No interim arrangements needed

- Delay was the main downside

Lesson: chains are less problematic when market confidence is high.

Key Takeaway

Being in a property chain is not inherently a problem, but it becomes a disadvantage in slower or uncertain markets. Breaking the chain can significantly improve your chances of success, but every option involves trade-offs, whether financial, logistical, or strategic.

There is no universal solution. The right approach depends on:

- Whether you need equity from your current home

- Your tolerance for short-term disruption

- Market conditions at the time

- Your long-term property plans

A clear strategy, considered early, can prevent delays, reduce stress, and avoid unnecessary compromises when moving home.

About the Author

Sekkappan Alagu is the Founder of Nachu Finance Ltd, established in 2006. With an early career in journalism and publishing, he brings clarity and structured thinking to complex financial topics. Through the Nachu Finance Blog and Knowledge Hub, he shares insights drawn from nearly two decades of client advisory experience, helping readers make informed decisions and understand best practices in mortgages, protection and long-term financial planning.

Business Profile

Nachu Finance Ltd is a directly authorised FCA-regulated firm providing mortgage, insurance and estate planning advice to clients across the UK. The firm takes a holistic approach — considering protection, tax efficiency and long-term planning alongside property finance — maintaining high regulatory standards while keeping advice clear and easy to follow. To learn more about the firm's background and story, visit the About Nachu Finance page.