Testmonials

Enquiry Form

Get in Touch with Us for Personalized Finance Assistance

Loan to Value and Equity Explained

A clear guide for homebuyers, covering purchase and remortgage scenarios

Loan to Value, often written as LTV, is one of the most common terms you will hear when discussing mortgages. Understanding it makes the rest of the mortgage process feel far more straightforward, as it helps you see clearly how much of the property is funded by the lender and how much is truly yours.

Below is a simple breakdown of the concepts of Loan to Value and Equity, how they are calculated, and why they matter.

What Does Loan to Value Mean?

Loan to Value represents the mortgage loan as a percentage of the property value.

If a property is worth £400,000 and the mortgage you need is £300,000, then:

300,000 ÷ 400,000 × 100 = 75% LTV

This means the lender is financing 75% of the property, and the remaining 25% represents your share. This share is your equity.

What Is Equity?

Equity is the portion of the property you own outright.

In pound terms:

Equity = Property value minus loan amount

In percentage terms:

Equity percent = 100 minus loan to value

Loan to Value and equity will always add up to 100%.

When buying a property equity would often be the deposit you put into the property.

Equity can come from various sources. It may be your own savings, a gifted deposit, a discount (such as Right to Buy), or equity gained over time through mortgage repayments and property value growth.

Why Loan to Value Matters

Mortgage lenders assess risk based on LTV. A higher LTV means the buyer is putting in a smaller share, therefore the lender is taking on a larger portion of the risk.

For example, if someone buys at 95% LTV and property prices fall by 10%, they could fall into negative equity. Lenders therefore tend to offer better interest rates to clients with a lower loan to value.

LTV also influences lending criteria. For example, a lender may cap the maximum LTV at 75% for certain types of applications. Lower LTV usually means better product availability and more competitive pricing.

Common LTV Bandings

Most lenders group their rates into LTV bandings. Although these vary slightly, the typical structure looks like this:

- 0 to 60% : often the most competitive rates

- 60 to 75%

- 75 to 85%

- 85 to 90%

- 90 to 95%

In the current market, the minimum deposit required for residential mortgages is usually 5%, meaning the highest LTV available tends to be 95%.

These bandings are used for pricing. Your exact deposit can be any figure that suits you, but the interest rate you receive will be based on the LTV band your case falls into.

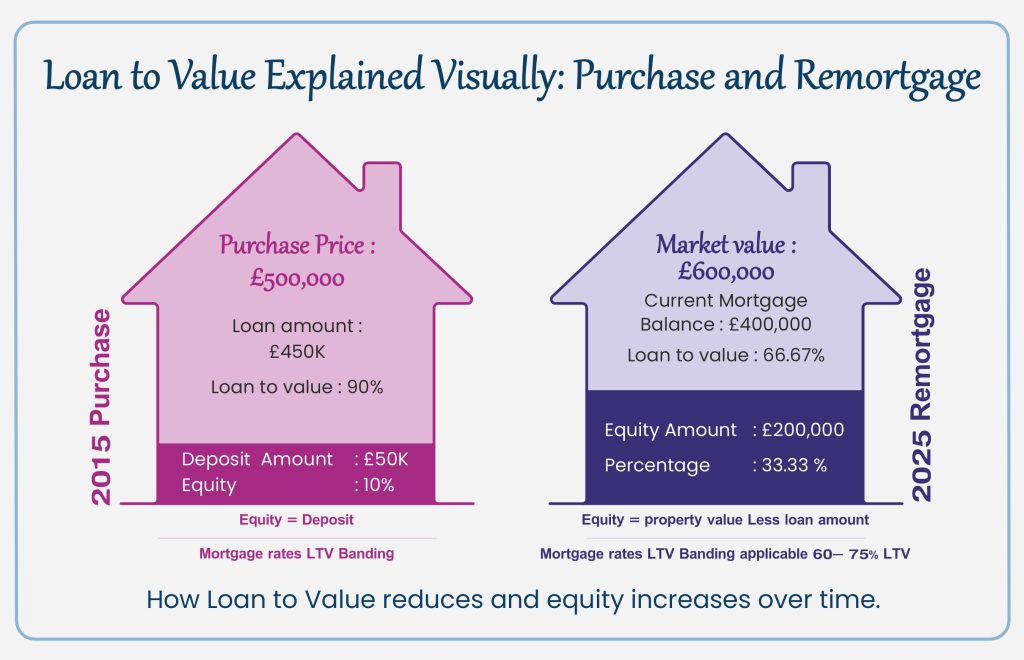

How LTV Works When Buying a Property

During a purchase, LTV is based on the deposit you put down.

Example:

Property price: £500,000

Deposit: £50,000

Loan amount: £450,000

LTV = 450,000 ÷ 500,000 × 100 = 90%

Equity = 10%

This applies even when the deposit is gifted. The key point is that the loan amount is lower, which reduces the LTV.

How LTV Works on a Remortgage

When remortgaging, there is no new deposit. Instead, equity comes from:

- How much of the mortgage you have already repaid, and

- Any increase in the property’s market value

Example:

Original purchase mortgage: £450,000

Ten years later, mortgage reduced to: £400,000

New property value: £600,000

LTV = 400,000 ÷ 600,000 × 100 = 66.67%

Equity is the remaining 33.33 percent, which is a combination of your repayments and market growth.

This is why many clients see their LTV improve over time, opening the door to better interest rates.

Equity does not always have to be savings.

In cases such as Right to Buy or family concessionary purchases, a discount can count as the deposit.

Example:

Right to Buy property value: £300,000

Right to Buy discount: £75,000

Mortgage required: £225,000

LTV = 225,000 ÷ 300,000 × 100 = 75%

Equity = 25%

Deposit provided physically by buyer = £0

The discount itself is treated as equity, helping the client meet mortgage criteria without having to save a deposit.

Similarly, in a family concessionary purchase where a parent sells a property to a child at below market value, the difference between the market value and the purchase price is often treated as gifted equity.

Frequently Asked Questions About Loan to Value

No. As a homebuyer, you are free to put down any deposit amount that suits your circumstances. The deposit does not have to be a neat rounded percentage such as exactly 10, 15 or 25% of the purchase price.

Loan to Value and equity percentages are calculated based on the deposit you put down, not the other way around.

For example, if you are buying a property worth £400,000, you do not need to restrict yourself to a £40,000 deposit (10%), £60,000 deposit (15%) or £100,000 deposit (25 percent). If you have £50,000 available, you can put down that amount as your deposit.

In this case:

Property price: £400,000

Deposit: £50,000

Loan: £350,000

LTV = 350,000 ÷ 400,000 × 100 = 87.5%

This would usually fall into the 85 to 90 %LTV band when it comes to selecting the interest rates. So while your deposit can be any amount, the product and interest rate offered will be based on the LTV banding into which your case falls.

This depends on whether it is a purchase or a remortgage.

- For a remortgage, the LTV is always based on the current market value of the property and the current mortgage balance. There is no purchase price involved at this stage.

- For a purchase, things are slightly different. In most straightforward cases, the purchase price and the market value are the same. However, there are situations where they may differ. For example:

- A buyer might pay more than the current market value because the property is in a very desirable location or is particularly convenient for them.

- A property might be bought below market value, for example at auction or in a distressed sale.

In these scenarios, lenders will usually calculate the LTV using the lower of the purchase price and the current market value.

So at the point of purchase, the LTV is typically:

Loan amount ÷ lower of (purchase price or current market value) × 100

This lower-of-the-two approach does not apply on a remortgage, because at that stage there is no new purchase price, only a current market value.

Bringing It All Together

Loan to Value and equity are two sides of the same concept. Together, they help determine:

- How much you can borrow

- The risk level for the lender

- The interest rate you are likely to be offered

- Your overall mortgage options

Once you understand these basics, interpreting mortgage products and criteria becomes much easier. The explanations and examples above are designed to give a clear, everyday understanding of how LTV works at purchase, at remortgage, and in special situations such as Right to Buy or concessionary purchases.

This knowledge hub article is intended simply to help you make sense of one of the most frequently used terms in mortgages.