Testmonials

Enquiry Form

Get in Touch with Us for Personalized Finance Assistance

Early Repayment Charges (ERC) – Explained Simply

- Date Published :

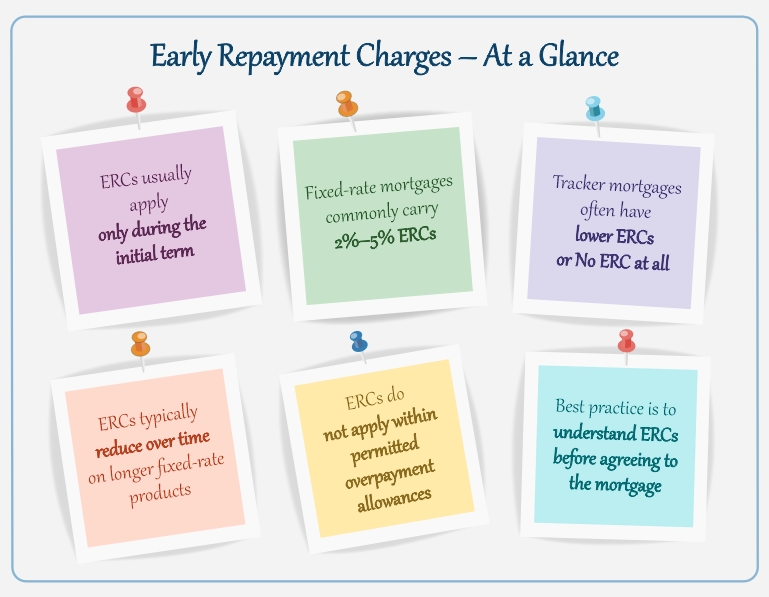

An Early Repayment Charge (ERC) is a charge payable to the lender if you repay, reduce, or switch your mortgage during the initial term of your mortgage product.

In simple terms, it is a penalty for exiting or reducing the mortgage earlier than agreed during the initial term.

When Does an Early Repayment Charge Apply?

ERCs usually apply only during the initial term of the mortgage. Once the initial term ends, you are typically free to:

- Repay the mortgage in full

- Switch to another lender

- Reduce the balance without penalty

During the initial term, lenders generally allow limited overpayments each year without triggering an ERC. If you exceed this allowance, an ERC may become payable on the excess amount.

Is There a Standard ERC?

No.

There is no fixed or standard ERC across lenders.

Early repayment charges vary based on:

- The lender

- The specific mortgage product

- The type of rate (fixed, tracker, etc.)

- The length of the initial term

This is why ERCs should always be reviewed alongside interest rates, arrangement fees, and monthly payments when choosing a mortgage.

Typical ERC Structures by Product Type

Two-Year Fixed Rate Mortgages

Common structures include:

- 2% throughout the entire two-year period, or

- Sliding scale, for example:

- 2% in year one

- 1% in year two

The exact structure depends on the lender and product.

Five-Year Fixed Rate Mortgages

Five-year fixed products often carry higher ERCs, reflecting the longer commitment. Common examples include:

- Up to 5% in the early years, reducing over time, or

- A fixed percentage applied throughout the five-year term

Some products use a sliding scale, while others apply a flat rate for the full period.

Tracker Mortgages

Tracker mortgages tend to be more flexible:

- Some tracker products are ERC-free, even during the initial term

- Others may have lower ERCs, such as 0.25%, 0.50% 1% etc

This flexibility is one reason trackers can be attractive where future changes are expected, but ERCs should still be checked carefully.

Examples of Early Repayment Charges (ERC) – Summary Table

![]()

Why ERCs Matter When Choosing a Mortgage

Early repayment charges are not just a technical detail. They can have a significant financial impact if:

- You plan to move home

- You expect a lump sum (bonus, inheritance, sale of assets)

- You intend to overpay aggressively

- Your circumstances may change

ERCs should always be assessed at the point of application, not as an afterthought.

Key Takeaway

An Early Repayment Charge is a normal part of many mortgage products, but it must be understood and accepted upfront. The right ERC structure depends on your plans, flexibility needs, and risk appetite.

About the Author

Sekkappan Alagu is the Founder of Nachu Finance Ltd, established in 2006. With an early career in journalism and publishing, he brings clarity and structured thinking to complex financial topics. Through the Nachu Finance Blog and Knowledge Hub, he shares insights drawn from nearly two decades of client advisory experience, helping readers make informed decisions and understand best practices in mortgages, protection and long-term financial planning.

Business Profile

Nachu Finance Ltd is a directly authorised FCA-regulated firm providing mortgage, insurance and estate planning advice to clients across the UK. The firm takes a holistic approach — considering protection, tax efficiency and long-term planning alongside property finance — maintaining high regulatory standards while keeping advice clear and easy to follow. To learn more about the firm's background and story, visit the About Nachu Finance page.