Testmonials

Enquiry Form

Get in Touch with Us for Personalized Finance Assistance

Insurance for Smokers: Know the Real Cost and Get the Right Cover

If you smoke—or have smoked in the past—your life insurance, critical illness, or income protection policy could cost significantly more than someone who has never smoked. But it doesn’t mean you can’t get good cover. What matters is understanding how insurers assess smoker status, how that impacts your premiums, and what steps you can take now to make informed decisions.

At Nachu Finance, we’re here to help you do just that—with tailored, transparent advice from across the market.

How Smoking Affects Your Insurance Premiums

Insurers view smoking as a serious health risk—and price their policies accordingly. This means:

- Smoker premiums are usually considerably higher than non-smoker rates.

- Even occasional or social smoking will place you in the smoker category.

- Premiums can vary not only between smoker and non-smoker but also between insurers—making the right adviser essential.

Who Counts as a Smoker?

Insurers have a broad definition of what makes someone a smoker. It includes:

- Cigarettes, cigars, and pipes (including shisha/hookah)

- Vapes and e-cigarettes

- Nicotine patches, gum, and other nicotine replacements

- Roll-ups or hand-rolled cigarettes

Even if you only smoke occasionally—at weddings, social gatherings, or under stress—you will be treated as a smoker.

Smoker Status Categories

Insurers broadly classify applicants as:

🔹 Non-Smoker (Never Smoked)

- No history of tobacco or nicotine use.

- Eligible for the lowest premiums.

🔹 Current Smoker

- Used nicotine in any form in the past 12 months.

- Subject to the highest premiums and possible medical underwriting.

🔹 Ex-Smoker (Quit Over 5 Years Ago)

- Treated like a non-smoker by most providers.

- No use of nicotine or related products in the last 5 years.

🔹 Previous Smoker (Quit Over 12 Months Ago but Less Than 5 Years)

- May receive mid-tier premiums—lower than current smokers, but not as low as non-smokers.

- Insurer criteria vary, so advice is essential.

➡️ We research the market to find insurers who take a more favourable view of your history and habits.

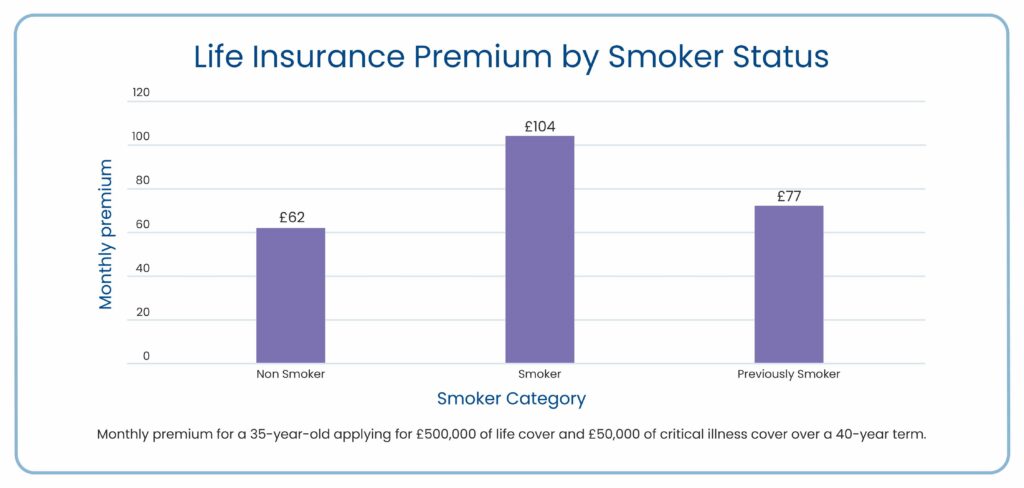

What Difference Does Smoking Make?

This chart shows how premiums can vary significantly based on smoker status—even when everything else remains the same.

For a 35-year-old applying for £500,000 of life cover and £50,000 of critical illness cover over a 40-year term:

- A non-smoker pays around £62/month

- A smoker pays over £104/month

- A Previous smoker pays £77/month

That’s a difference of more than £500 per year, and over £1,600/year between the lowest and highest categories if critical illness were increased.

The message is clear: quitting smoking can improve not only your health—but also your financial protection.

Cotinine Testing: Can Insurers Verify Your Status?

Yes. Some insurers may require a cotinine test (which detects a nicotine by-product in your urine or blood), especially when:

- The cover amount is high

- You are older at the time of application

- Or at the insurer’s discretion

Being transparent from the start avoids complications later.

The Importance of Truthful Declarations

Being honest on your application isn’t just good practice—it’s essential.

If you inaccurately declare your smoker status, the insurer may:

- Refuse to pay out a future claim

- Cancel the policy

- Delay processing during a difficult time for your loved ones

At Nachu Finance:

- We guide you through the disclosure process

- Review your application with you before submission

- Ensure the insurer receives accurate and complete information

We don’t believe in shortcuts—only in getting it right.

What If You Start or Stop Smoking Later?

The future is unpredictable—and that’s exactly why insurance exists: to protect you against unforeseen events down the line.

Once your insurance policy goes live, any changes to your health, lifestyle, or smoker status do not impact the terms or premiums of your existing policy. This means:

- If your health worsens after the policy starts, you remain fully covered under the terms agreed at the outset.

- If you start smoking later, your premiums stay the same, and you are not required to inform the insurer.

- If you quit smoking after your policy goes live, you won’t automatically get lower premiums—but you can apply for a new policy to see if better terms are available once you’ve been nicotine-free for a qualifying period.

This approach gives you certainty and peace of mind, knowing that your cover won’t change—even if your circumstances do.

Keep Your GP Records Updated

Your GP records can play an important role in insurance assessments—particularly when you’re applying for new cover or reviewing an existing policy.

- If you quit smoking, make sure your GP updates your records with the correct date you stopped. This can support future applications or reviews when you’re hoping to qualify for non-smoker rates.

- If you were a non-smoker at the time of your original application and later become a smoker, it’s also best to inform your GP of the date you started. While this won’t affect your existing policy, accurate medical records matter—especially if you apply for additional cover later or go through a claims process involving health records.

At Nachu Finance, we always advise our clients to ensure their medical history is up to date and consistent, so there are no surprises when it matters most.

Why Quitting Makes Financial Sense Too

Beyond health benefits, quitting smoking can save you thousands over the life of your policy.

Many of our clients who stopped smoking:

- Revisited their insurance after 12 months or more

- Reduced their premiums

- Or increased their cover for the same price

It’s a great incentive to kick the habit.

How Nachu Finance Helps Smokers

We go beyond simply finding you a quote. Our process is tailored to your situation:

✅ Pre-application research to match you with the right insurer

✅ Clear explanations of smoker status and how it affects your policy

✅ Support throughout the application and underwriting process

✅ Regular reviews to reassess your status and update your protection if needed

✅ Whole-of-market advice—not limited to just a few providers

Whether you smoke regularly, socially, or have recently quit, we make sure your policy is suitable, sustainable, and secure.

Our Transparency Promise

Truth Today. Peace of Mind Tomorrow.

At Nachu Finance, we’re proud to be transparent—even when it’s not the cheapest route upfront.

We’ll always encourage you to:

- Declare your smoker status truthfully

- Understand what the insurer will and won’t cover

- Prioritise a policy that will pay out without questions when your family needs it

Yes, this might mean slightly higher premiums now. But it also means genuine peace of mind later.

We take time to review your application with you, so you feel confident that everything is in order—no surprises, no uncertainty.

Because if a policy won’t pay out, what’s the point of having one?

Ready to Find the Right Cover—Whatever Your Smoker Status?

If you’re a smoker, an ex-smoker, or someone thinking about quitting, let us help you take the next step with:

- Honest advice

- Whole-of-market access

- A personalised, professional approach

Contact Nachu Finance today for a free, no-obligation consultation.

We’ll help you secure the protection your family deserves—with clarity, care, and confidence.

📞 Call us or 📩 get in touch online to get started.