Within the CIS mortgage scheme, the last three months’ average income plays a crucial role in determining mortgage affordability. Lenders already assume that CIS workers can only work 46 weeks per year, meaning they multiply the weekly average by 46 rather than 52.

If the last three months’ gross earnings (as evidenced by invoices) do not accurately reflect a CIS worker’s full earning potential, the calculated income may be lower, directly impacting the maximum loan available.

Overcoming the Common Challenges with the Last Three Months’ Income

From our experience, two key issues frequently arise when CIS workers apply for mortgages:

Festive Breaks – If applying for a mortgage in January or February, the last three months’ income may be lower due to the December holiday period, as many CIS workers take time off in the later part of the year.

Property Viewings & Time Off Work – We often see cases where the initial income snapshot looks strong, but by the time clients have viewed properties, made offers, and had an offer accepted, their income has dropped. If time off work for property viewings reduces invoice values, it can affect the loan amount available.

To maximise borrowing potential under the CIS scheme, it’s important to ensure that the three months leading up to the mortgage application accurately reflect full earning capacity.

To apply for a mortgage under the CIS scheme, lenders require the following:

For Income Assessment

- Last three months (13 weeks) of CIS invoices

- Last three months’ bank statements, showing net CIS payments from the employer to the subcontractor

Important: The CIS invoices and bank statements must cover the same period to allow the lender to verify and corroborate the income accurately. This ensures that the lender can match invoiced earnings with actual payments received, strengthening the mortgage application.

For Compliance Requirements

Self-employed accounts (for sole traders or Ltd companies) may also be required.

While this is not used for affordability calculations, it is needed for compliance purposes.

If the document is unavailable for a valid reason, we may still proceed, but lenders will require either the document itself or an explanation for its absence.

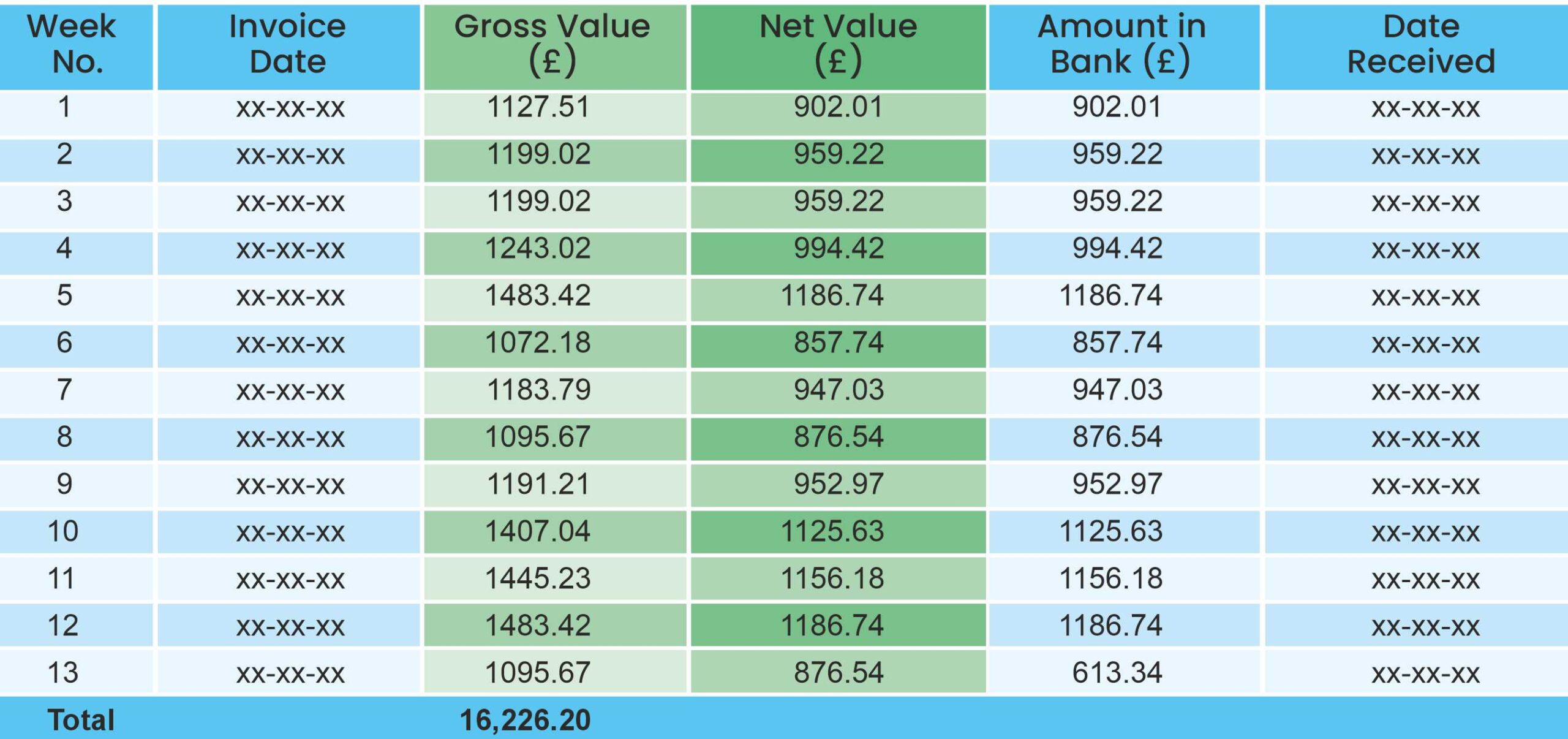

To illustrate how income is assessed under the CIS mortgage scheme, here’s a sample calculation based on 13 weeks of invoices.

Calculation Breakdown:

Total Gross Income (A) over 13 weeks: £16,226.20

Weekly Average Income: £1,248.17 (A ÷ 13 weeks)

Annualised Income: £57,415.80 (A ÷ 13 × 46 weeks)

This approach allows lenders to assess CIS workers’ true earning potential without relying on traditional self-employed tax returns, which may understate their actual income.

A 30 & 29-year-old couple were looking to purchase their first home.

Mrs: A newly qualified professional earning £42,000 per year (PAYE).

Mr: A CIS worker employed as a site engineer with a daily rate of £275 and working 5.75 days per week.

Mr operates via a Ltd company and receives net CIS income from his employer.

Income Comparison

Key takeaway: The self-employed income of £44,360 was insufficient for their mortgage, but the CIS-calculated income of £71,318 enabled them to secure the loan needed for their dream home. Without the CIS mortgage scheme, they would not have been able to proceed with their property purchase.

A couple wanted to remortgage their residential property and release £75,000 for home improvements.

Mrs: Works in retail, earning £23,000 per year (PAYE).

Mr: A carpenter who moved into the CIS scheme nine months ago, using a sole trader structure to receive net CIS income.

Challenges & Solution

Before CIS: As Mr was previously employed (PAYE) and had less than a year of self-employed accounts, traditional mortgage lenders would not have considered his income.

With CIS: We leveraged his last three months’ CIS income since he had over five years of experience as a carpenter, which met the lender’s minimum requirement of two years in the trade.

Outcome: The remortgage was successfully completed, and the couple secured the £75,000 needed for home improvements. Without the CIS mortgage scheme, they would have needed at least one (or ideally two) years of self-employed accounts before lenders would consider their income.

A steel fixer was recently promoted to a supervisor, increasing his day rate by 24%.

Challenges & Solution

Before CIS: Despite having two years of self-employed accounts, these accounts did not reflect his recent salary increase.

With CIS: Instead of using outdated accounts, we applied for a mortgage using his last three months’ CIS invoices, which accurately reflected his new earning capacity.

Outcome: The CIS income assessment played a vital role in securing a mortgage amount that matched his true earnings, allowing him to move forward with his property purchase.