Testmonials

"The entire team was very professional and proactive, making the whole process smooth and easy for us."

Ilford

First-time buyer

"He always presents options that suit my financial situation and helps me make informed decisions."

Leamington Spa

Remortgage client

"Sekkappan and the team were always on hand to answer our questions, and they followed up on everything promptly."

Hertfordshire

Remortgage client

"The service, advice, and support have always been consistent. Every email and call has been answered promptly."

Middlesex

Portfolio landlord

"Thanks to Sekkappan, we saved money on our mortgage and felt supported throughout."

Worcester

Home mover

"Sekkappan and his team took ownership of our requirements and guided us through every stage."

Aylesbury

Home buyer

"Sekkappan made the complex mortgage process feel like a cakewalk."

Croydon

Home buyer

"Their meticulous attention to detail and genuine care for our financial goals were truly appreciated."

Essex

Home buyer

Enquiry Form

Get in Touch with Us for Personalized Finance Assistance

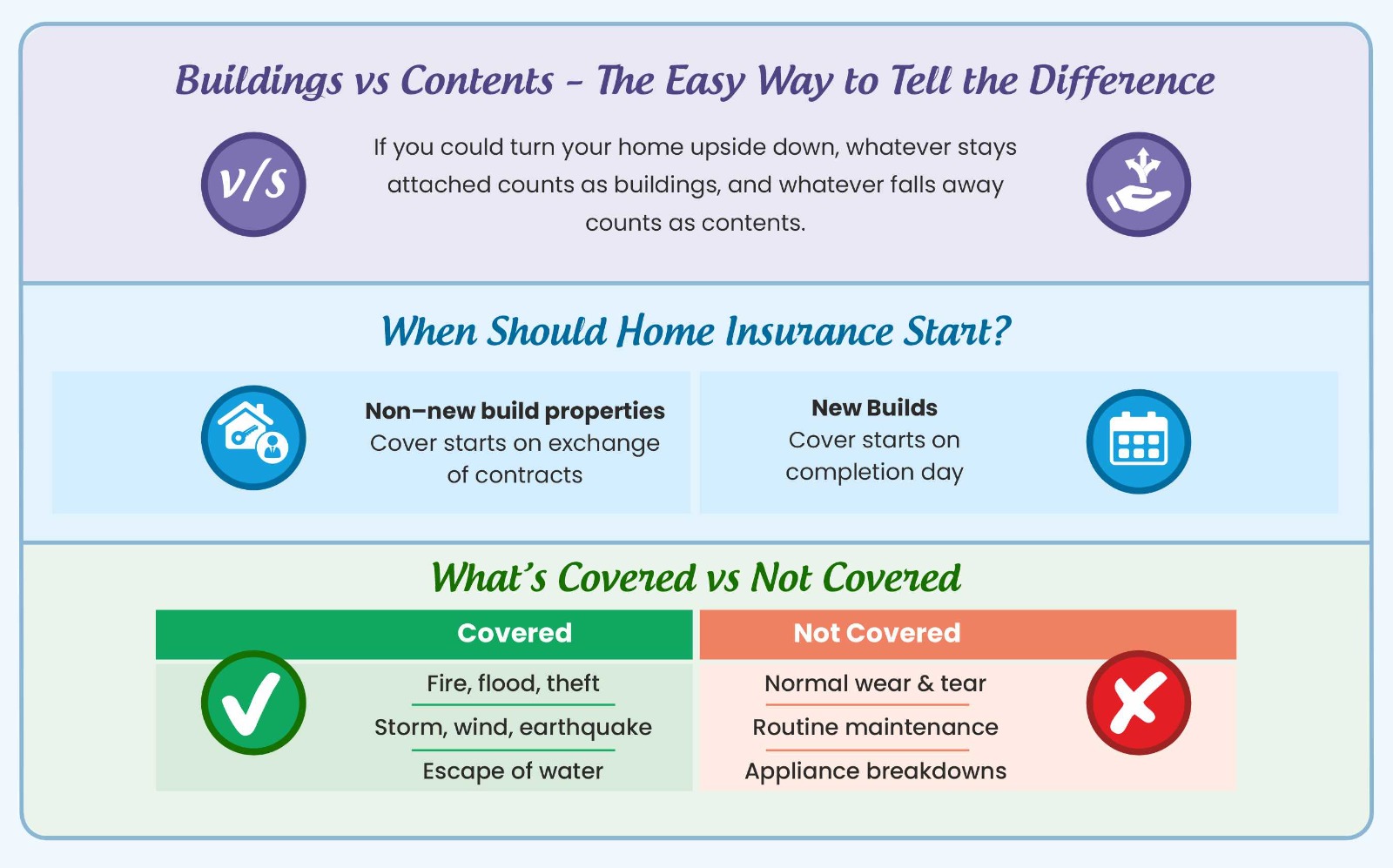

What Is Buildings & Contents Insurance?

Buildings and contents insurance protects your property and everything that makes it a home.

When purchasing a property with a mortgage, buildings insurance is mandatory, as the mortgage lender has a financial interest in the property. They want to ensure that in the event of damage caused by fire, flood, storm, or similar unforeseen events, the property can be repaired or rebuilt.

Contents insurance, on the other hand, is optional. It protects your belongings such as furniture, clothes, electronics, and valuables against damage or theft. While not compulsory, it is a prudent choice to safeguard your possessions against unexpected events.

What Does Home Insurance Cover (and Not Cover)?

Home insurance is designed to protect you from unforeseen and external events — for example:

- Fire, flood, storm, or earthquake damage

- Theft or attempted break-ins

- Vandalism or malicious damage

- Subsidence or escape of water (depending on policy)

However, home insurance does not cover normal wear and tear, day-to-day repairs, or the mechanical breakdown of appliances.

The key idea is that it protects against unexpected external damage, not general maintenance.

When Should the Insurance Start?

For most existing (non–new build) properties, buildings insurance should start from the date of exchange of contracts.

At that point, you become legally bound to complete the purchase, and if anything happens to the property between exchange and completion, you would still be responsible.

For new build properties, where the home is not yet complete at exchange, the cover usually starts on completion day. Any damage before completion would be covered under the developer’s own insurance policy.

Understanding the Sum Assured

The buildings sum assured is based on the rebuild cost — not the market value.

This means the amount required to clear debris and rebuild the property from scratch, should the worst happen.

While earlier insurers used detailed calculators to estimate rebuild costs, many providers today apply a minimum sum insured, usually between £500,000 and £1.5 million, depending on the type of cover.

Even if your actual rebuild cost is lower, premiums are typically set for a range, so reducing the sum insured may not reduce the premium.

For contents insurance, the total cover is based on the replacement value of all your possessions as new — not their current used value. Some insurers classify levels of cover as Bronze, Silver, or Gold, with corresponding cover amounts (for example, £25,000, £50,000, or £75,000).

Valuables such as jewellery, watches, antiques, and art often have their own category. If you have items of higher value, these need to be declared separately to ensure they are covered correctly.

Monthly vs Annual Premiums

While insurers offer both monthly and annual payment options, annual payments often work out more economical.

Monthly payments typically include an interest element and may slightly increase the overall cost.

Where possible, we recommend paying annually by direct debit or debit card. This keeps your monthly outgoings lower and ensures the policy remains active without interruption.

Flats and Leasehold Properties

If you are buying or owning a flat, the buildings insurance is usually arranged by the freeholder or management company and included within your service charge.Your solicitor should confirm this as part of the legal checks.

For flat owners, it’s still advisable to arrange contents-only cover to protect your personal belongings inside the property.

At Nachu Finance, when arranging cover for flats, we focus on contents insurance and guide you to confirm that the building element is included in the service charge.

Renewal and Reviewing Your Policy

Home insurance policies are typically valid for one year, with renewal invitations issued about a month before expiry.

It is always sensible to review your renewal quote — if the price appears reasonable, you can continue with the same provider; otherwise, it may be worth obtaining new quotes from alternative insurers.

If you engage Nachu Finance, we can review your renewal quotes to ensure you’re getting a competitive and suitable level of cover.

The Nachu Finance Way

At Nachu Finance, home insurance is not just a tick-box exercise.

We provide a matrix of options from across the market — normally including both buildings and contents cover unless you request otherwise.

Each quote includes:

- Building and contents sum assured

- Monthly and annual premium comparison

- Policy highlights from reputable insurers

- Detailed illustration for the most competitive cover

This transparent approach helps you understand not only the cost but also the quality of cover and provider reputation.

Keeping Records of Valuable Items

As a matter of best practice, we encourage clients to maintain evidence of ownership for valuable items such as jewellery, watches, antiques, and high-value electronics.

Having clear proof makes it easier to support a claim or a police report if items are lost, stolen, or damaged.

Where possible:

- Keep purchase receipts or invoices for valuable items.

- Take clear photographs showing the item and any identifying features or certificates.

- Store these records electronically, for example in secure cloud storage or an email folder, so they can be retrieved easily if ever required.

This small step can save considerable time and stress in the event of a claim and ensures that your policy works exactly as intended when you need it most.This practice is also helpful if you ever change insurers, as it provides a clear record of your items’ ownership and condition.

Summary

- Buildings insurance is mandatory if you have a mortgage.

- Contents insurance is optional but strongly recommended.

- Cover starts at exchange (for Non–new build properties) or completion (for new builds).

- Policies are based on rebuild cost and replacement value.

- Annual payments are usually cheaper than monthly.

- Flat owners should ensure buildings cover is included within the service charge.

- Always review renewals and check if your policy remains competitive.

Yes, you can, but most insurers may apply a cancellation fee. It’s often best to review your options at renewal unless there’s a significant issue or pricing concern.

Always inform your insurer or adviser if you extend, renovate, or make major alterations. These can affect the rebuild cost and, in turn, your insurance validity.

Contact your insurer as soon as possible after an incident. They’ll request details, evidence, and photographs. Your adviser can guide you on what information to prepare for a smoother process.

The excess is the portion of a claim you pay yourself before the insurer covers the rest. Choosing a higher excess can slightly reduce your premium but increases your out-of-pocket cost at claim time. When comparing policies make sure you take into account the excess applicable.

Yes. Most policies offer this as an optional add-on. It can be worthwhile for families, landlords, or anyone wanting broader protection against unintentional damage inside the home.

If your property will be unoccupied for more than 30 days, you must inform your insurer. Different conditions or exclusions may apply during that period.

Yes, it’s best practice for both property owners to be named on the home insurance policy.This ensures that both owners are covered for any claims and that the policy accurately reflects the ownership structure.If only one person is named, it may lead to complications in a future claim

Our Transparency Promise

Not Afraid to Tell You the Truth

While we use our experience and relationships to secure strong quotes, it’s possible that online comparison websites may show cheaper options.

We believe in being upfront about this. Our focus is on quality, reliability, and ensuring the policy is right for your situation rather than just chasing the lowest cost.

Join Our Happy Clients Today

We primarily arrange home insurance as part of a wider holistic service — typically alongside your mortgage, life insurance, or estate planning.

Standalone home insurance is not our main service line, but if we are already supporting you with your mortgage or protection, we’ll be happy to arrange suitable home insurance as part of the overall solution.